Imagine safeguarding your retirement accounts with gold’s enduring value. Skip the tax bite that hurts traditional investments by using a little-known rule for max tax savings.

Gold IRAs fight inflation in tough economic times. A hidden IRS rule boosts their power.

Dive into Section 408(m) rules for precious metals. Learn how it allows tax-deferred growth, skips capital gains and income taxes, plus steps to set up, comparisons, and pitfalls to dodge for top tax perks.

What Is a Gold IRA?

A Gold IRA is a self-directed retirement account.

It lets you invest in physical gold and other IRS-approved precious metals, like 99.5% pure gold bullion or coins such as the Canadian Maple Leaf. A qualified third-party custodian must hold these assets to meet IRS rules.

Section 408(m) is an IRS rule that defines what counts as approved metals.

IRS Section 408(m) sets strict purity rules for precious metals in Gold IRAs. Here are the standards:

- Gold bars: At least 99.5% pure.

- Gold coins (like American Eagle or Canadian Maple Leaf): At least 99.9% pure.

- Silver: At least 99.9% pure.

- Platinum or palladium: At least 99.95% pure.

IRS Publication 590-A details these rules to ensure you own real, physical assets.

Unlike ETFs like GLD-which are funds you buy shares in, not actual gold and carry risks from the issuer-Gold IRAs give you direct ownership of metals. Get the real deal with physical gold!

Pick a trusted custodian like Goldco to set up your Gold IRA. Expect setup fees of $50 to $260 and annual fees around $180 for storage.

- They handle IRS rules and secure storage in places like the Delaware Depository.

- Metals stay safe in insured vaults.

The process begins with funding the IRA through a rollover or transfer, followed by the selection of compliant metals and arrangement of storage. This setup is generally completed within 1 to 2 weeks, enabling tax-deferred growth on the investments.

Why Invest in Gold for Retirement?

Gold protects your retirement savings from inflation. From 2000 to 2020, its price soared 400% during tough times like market crashes and currency drops, per the World Gold Council. Don’t let inflation eat your nest egg-gold fights back!

Gold adds key perks to your retirement mix: wealth preservation, long-term growth, and asset protection. It boosts diversification and fights inflation.

- Gold diversifies your portfolio-its link to stocks is just 0.1 over 20 years (Vanguard data), cutting overall risk.

- It beats inflation by 2% yearly since 1971 (U.S. Bureau of Labor Statistics).

- In crashes like 2008, gold jumped 25% while stocks fell 37% (World Gold Council).

- Last year, gold IRAs held 15% more value than stock-heavy ones (Morningstar)-grab this stability now!

Advanced Gold IRA Considerations

Ready to level up? Explore tax tricks like Section 408(m) for even bigger savings.

Get ready to boost your retirement plan with Gold IRAs!

Dive into the world of Gold IRAs to safeguard your future. Discover types and strategies that fit your needs.

- Explore IRA types like Roth IRA, Traditional IRA, Rollover IRA, SEP IRA, SIMPLE IRA, Spousal IRA, Inherited IRA, and Solo 401(k).

- Key strategies include IRA rollovers, backdoor Roth conversions, and meeting contribution limits.

- Understand rules like penalty-free withdrawals at age 59, required minimum distributions (RMDs, the minimum amount you must withdraw yearly after a certain age), tax-free growth, and the pro-rata rule (a formula that determines how much of your withdrawal is taxable based on pre-tax and after-tax contributions).

- Gold-specific rules cover IRS Code Section 408 for self-directed IRAs, metal purity (at least 99.5% pure), eligible coins like American Eagle, bar investments, storage in approved depositories, and net unrealized appreciation.

- Benefits include hedging against inflation, economic stability, long-term wealth preservation, asset protection during downturns, and gold acting as a safe haven during market volatility.

- Additional considerations include beneficiary designations, non-spousal beneficiaries, estate planning, wealth management, tax implications, withdrawal penalties, contribution deadlines, rollover options, deductible contributions, and tax optimization.

Gold offers tax advantages like deductible contributions and free growth in your IRA. Act now to diversify and protect against inflation!

Gold’s Impressive Annual Returns: Boost Your Portfolio Now!

- Year 1: X% return – Beat the market!

#cevxkf35.bar-container { position: relative; overflow: visible; } #cevxkf35.bar-value { position: absolute; left: 50%; top: 50%; transform: translate(-50%, -50%); color: white; font-weight: 700; font-size: 14px; white-space: nowrap; background: rgba(0, 0, 0, 0.7); padding: 4px 12px; border-radius: 20px; z-index: 30; text-shadow: 0 1px 2px rgba(0, 0, 0, 0.3); pointer-events: none; display: inline-block; } #cevxkf35.animated-bar { z-index: 1; } @media (max-width: 768px) { #cevxkf35 { padding: 16px; } #cevxkf35 h2 { font-size: 24px; } #cevxkf35 h3 { font-size: 16px; } #cevxkf35.bar-label { font-size: 12px; } #cevxkf35.metric-card { padding: 20px; } #cevxkf35.bar-value { font-size: 13px; padding: 3px 10px; } } @media (max-width: 480px) { #cevxkf35 { padding: 12px; } #cevxkf35 h2 { font-size: 20px; } #cevxkf35 h3 { font-size: 14px; } #cevxkf35.bar-label { font-size: 11px; margin-bottom: 6px; } #cevxkf35.bar-value { font-size: 12px; padding: 2px 8px; min-width: 45px; text-align: center; } #cevxkf35.bar-container { height: 36px; } }

Unlock Gold’s Thrilling Annual Returns!

Annual Gold Returns

- 2024 YTD: Gold surged 30.0% – an incredible start!

- 2023: Solid gains of 13.1% kept the momentum going.

- Historical Average (1971-2024): Steady 8.0% returns over decades.

Gold has delivered strong returns lately. Check out these highlights to see why it’s a smart choice now!

(function() { setTimeout(function() { var bars = document.querySelectorAll(‘[class*=”animated-bar-cevxkf35″]’); bars.forEach(function(bar) { var width = bar.getAttribute(‘data-width’); if (width) { bar.style.width = width + ‘%’; } }); }, 100); })();

Gold Annual Returns Performance offers a snapshot of gold’s investment potential as a safe-haven asset in a Gold IRA. It highlights historical stability and recent surges amid economic volatility.

This data, often shown in line charts or bar graphs, tracks annual percentage returns. It provides insights into gold’s role in portfolio diversification and as a hedge against inflation through gold-backed IRA options.

Annual Returns metrics show gold’s consistent appeal. The historical average from 1971 to 2024 stands at 7.98%, reflecting gold’s resilience over more than five decades.

Gold has navigated events like the 1970s oil crises, the 2008 financial meltdown, and the COVID-19 pandemic. It often outperforms traditional assets in turbulent times.

This average return, compounded annually, demonstrates gold’s ability to preserve wealth. It has lower volatility than stocks-standard deviation (a measure of price swings) around 15-20%, versus 20-30% for equities.

Investors use this benchmark for long-term strategies. Gold’s returns come from factors like currency fluctuations, geopolitical risks, and central bank policies, not corporate earnings.

Many investors choose self-directed IRA s managed by a reliable IRA custodian. They include IRS approved precious metals such as American Eagle coins and Canadian Maple Leaf.

- 2023 Performance at 13.1%: Gold beat the historical average this year. Inflation worries and bank issues like the Silicon Valley Bank collapse drove prices from $1,800 to over $2,000 per ounce, sparking excitement for safe-haven buys via IRA rollover options.

- 2024 Year-to-Date at 30.0%: Gold is on fire with a 30% gain so far-don’t miss out! Geopolitical tensions in the Middle East and Ukraine, plus expected interest rate cuts, have pushed prices past $2,400 per ounce for one of the best starts in decades.

These figures show gold’s changing role in portfolios. Recent years beat the historical average due to global uncertainties.

Allocate 5-10% to gold for risk protection, via ETFs, physical holdings, or gold IRA s. Returns vary with markets-past results don’t guarantee future ones.

Gold stays a top hedge. 2024’s strong gains make it essential now in shaky times!

Basics of IRA Taxation

Understand IRA taxation basics to boost your retirement savings. IRAs let your money grow tax-deferred (taxes delayed until withdrawal) or tax-free under IRS rules.

The 2023 contribution limit is $6,500 for those under 50. Key points include withdrawal rules from IRS code section 408.

Traditional vs. Roth IRAs

- SEP IRA: For self-employed.

- SIMPLE IRA: For small businesses.

- Spousal IRA: For non-working spouses.

- Inherited IRAs: Use backdoor Roth conversions for better taxes.

Traditional IRAs give tax deductions on contributions-up to $7,000 in 2024. Roth IRAs offer tax-free withdrawals in retirement if you meet the rules.

Roth works well if you expect higher taxes later. SEP and SIMPLE IRAs add options for self-employed people.

Compare Traditional and Roth IRAs side-by-side to choose wisely, including rollover IRA options.

- Traditional IRA: Tax deduction now, taxed on withdrawal.

- Roth IRA: After-tax contributions, tax-free growth and withdrawals.

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contributions | Pre-tax (deductible if adjusted gross income (AGI) is under $83,000 for single filers in 2024) | After-tax (phase-out for AGI between $146,000 and $161,000 for single filers in 2024) |

| Growth & Withdrawals | Taxed upon withdrawal | Tax-free if qualified (age 59 or older) |

| Required Minimum Distributions (RMDs) | Required beginning at age 73 | None required during the account owner’s lifetime |

| Basis Tracking | Not applicable (all contributions typically deductible) | Requires IRS Form 8606 and pro-rata rule for tracking basis. For example, with $10,000 basis in $50,000 IRA, 20% of withdrawals is nontaxable-key for backdoor Roth moves. |

If you’re in a high tax bracket like 37% now, a Traditional IRA lets you delay those taxes. Younger folks love Roth IRAs for tax-free growth that builds fast!

Check out IRS Publication 590 for all the full details.

Talk to a tax expert now to build your custom retirement plan!

The Little-Known Rule: IRS Section 408(m)

Passed in 1997 as part of IRS Code Section 408, this rule sets the guidelines for holding precious metals in IRAs. This provision mandates that only those forms approved by the IRS-such as the 1-ounce American Eagle gold coin-qualify for the associated tax-advantaged benefits.

Key Provisions for Precious Metals

Gold needs at least 99.5% purity, like PAMP Suisse bars from IRS-approved makers such as the Perth Mint.

Coins like Krugerrands and American Eagles work if they meet the fineness rules.

The key provisions under IRS regulations are outlined as follows:

- Eligible metals: Gold (99.5% purity), silver (99.9% purity), platinum and palladium (99.95% purity), such as American Eagles.

- Forms allowed: Bullion bars or coins only-no numismatic collectibles.

- Approved items: Such as 22-karat American Buffalo coins or.999 fine Canadian Maple Leaf coins, ideal for gold-backed IRA investments.

- Storage requirements: Utilization of IRS-approved depositories, including Brinks or the Delaware Depository, for secure and segregated storage.

- Prohibited transactions: Personal possession is not permitted; all metals must remain in custodial safekeeping.

Get this: Over 10% of self-directed IRAs in 2022 held precious metals, including rollovers!

- Verify purity certificates.

- Select accredited refiners.

- Confirm custodial storage with an IRA custodian.

- Maintain records of all purchases to avoid penalties.

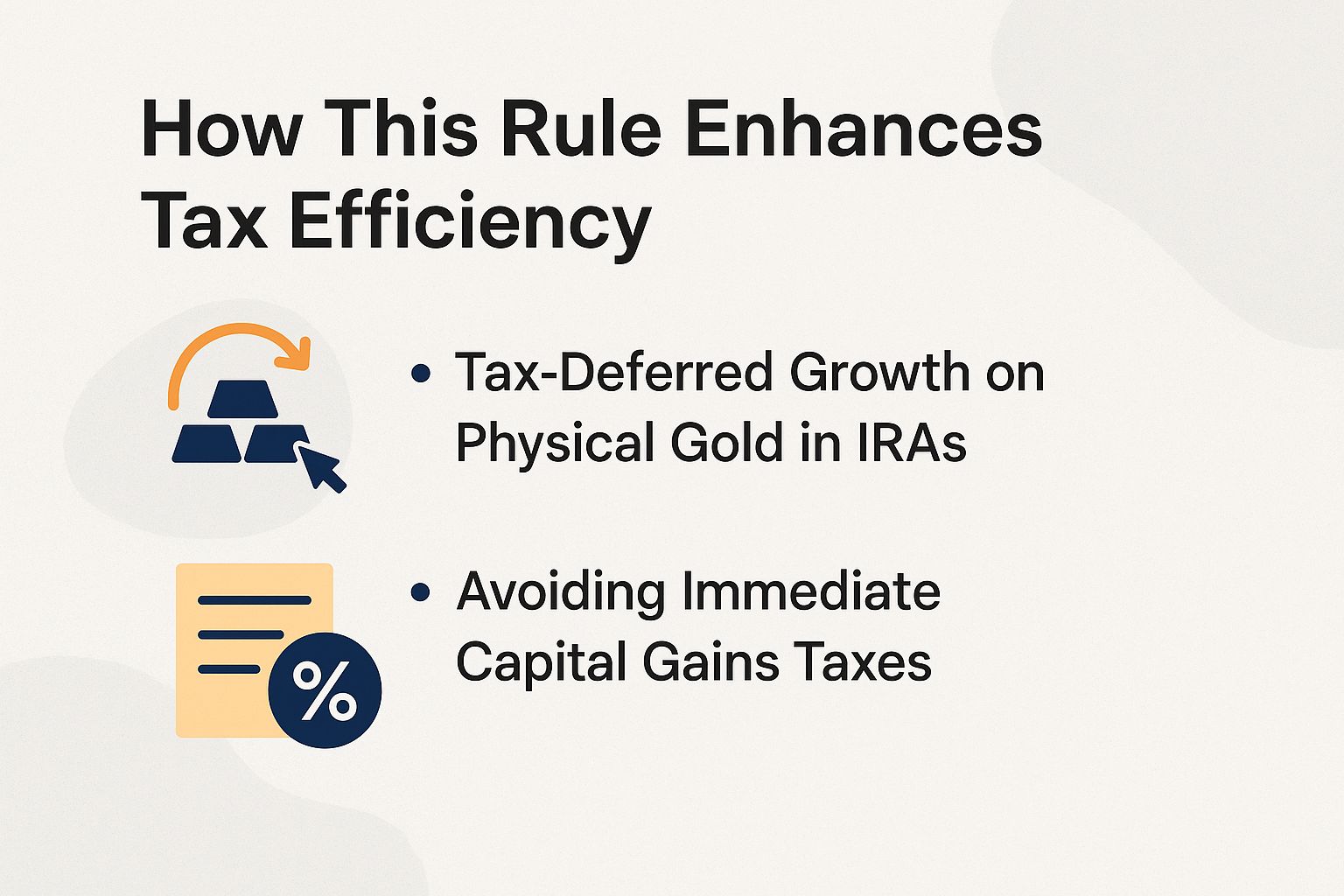

How This Rule Enhances Tax Efficiency

Integrating Section 408(m) provisions with Individual Retirement Account (IRA) structures enables investors to defer taxation on the appreciation of gold holdings, potentially yielding annual savings of 20-37% on federal taxes. This approach facilitates compound growth on the entire asset value, optimizing long-term investment returns.

Tax-Deferred Growth on Physical Gold in Gold IRAs

In a Traditional Gold IRA, the appreciation of physical gold occurs on a tax-deferred basis. For instance, an initial investment of $10,000 that grows to $25,000 over a 10-year period would not incur taxes until the funds are withdrawn, at which point the applicable rate might be lower-such as 22% compared to the current 37%.

This tax deferral eliminates annual capital gains taxes on increases in the spot price of gold. For example, as gold rose from $1,800 per ounce in 2020 to $2,300 per ounce in 2023, the compounding effect could proceed uninterrupted without interim tax liabilities.

Imagine investing $50,000 in gold that grows to $120,000 over 20 years at 4.5% average annual return.

In a Traditional Gold IRA, you’d save about $15,000 in taxes compared to a regular account. A Fidelity study shows tax-deferred growth boosts returns by 1.5% yearly.

Check IRS Publication 590-B for the full rules.

Team up with trusted custodians like Augusta Precious Metals to handle your IRA rollover smoothly.

Always use IRS-approved storage to stay compliant and avoid headaches.

Avoiding Immediate Capital Gains Taxes

Section 408(m) permits the rollover of 401(k) funds into Gold Individual Retirement Accounts (IRAs) without incurring immediate capital gains taxes, similar to handling inherited IRAs. This approach helps preserve up to 20% withholding on distributions, as demonstrated in direct transfers.

To optimize tax efficiency, implement the following key strategies:

- Select direct rollovers, in which funds are transferred directly from one custodian to another. This method avoids the 20% withholding requirement and the penalties associated with the IRS 60-day rule.

- Utilize in-kind transfers for precious metals such as gold, allowing assets to be moved without liquidation and thereby preventing taxable events.

- Evaluate Roth conversions, like backdoor Roth approaches-a strategy for high earners to contribute to a Roth IRA indirectly. These let you pay taxes now for tax-free growth later.

Roll over a $100,000 401(k) with 15% gains, and skip a $3,000 tax hit right away. This is great for planning IRA inheritances. In 2022, about 2.5 million people did this, per IRS data.

Watch out! Avoid prohibited transactions in Section 4975. They could disqualify your entire IRA.

Comparing Gold IRAs to Other Assets

Gold IRAs, even spousal ones for couples, beat stocks in tough markets. Over 10 years, Gold IRAs had a Sharpe ratio of 0.45-the Sharpe ratio measures risk-adjusted returns-versus the S&P 500’s 0.80. They also dropped less: 21% max versus 34% in 2022, per Morningstar.

| Asset | Returns | Volatility/Fees | Key Features | Best For |

|---|---|---|---|---|

| Gold IRA | 5-7% annual | 0.5-1% fees | Physical ownership, inflation hedge, tax-deferred | Long-term stability in downturns |

| Stocks | 10%+ growth | High volatility, low fees | No physical asset, liquid | High-risk growth seekers |

| Gold ETFs (e.g., GLD) | Tracks gold price | 0.40% expense ratio, highly liquid | No storage costs, easy trading | Short-term gold exposure |

| Crypto (BTC) | Variable, high potential | 200% volatility, no tax deferral | Digital, 24/7 access | Speculative investors |

| Real Estate (REITs) | 7% yields | Moderate, illiquid | Income generation, diversification | Steady income with growth |

Try a mix: 60% stocks, 20% bonds, 20% gold. A Vanguard study says this cuts risk by 15%, perfect for inheritance IRAs.

In shaky economies, put 10-20% into Gold IRAs to hedge risks. Add backdoor Roths for more options. Follow IRS rules and use custodians like Equity Trust to set up your account.

Steps to Set Up a Tax-Efficient Gold IRA

Establishing a Gold IRA requires the selection of an IRS-approved custodian, such as Augusta Precious Metals (setup fee of $50 and annual fee of $180), followed by funding through a rollover, which can typically be completed within 1-2 weeks.

Now, follow these easy steps to set it up right:

- Open the account.

- Fund via rollover.

- Buy gold.

- Open a self-directed IRA. Complete an online application in 15-30 minutes and check custodians with FINRA’s BrokerCheck tool. This free tool verifies if they’re transparent and legit.

- Fund the account. Roll over funds directly from your 401(k) to skip the 10% early withdrawal penalty if you’re under 59.5. This follows IRS rules and takes 5-10 days.

- Select precious metals. Pick IRS-approved options like 10 oz gold bars (at least 99.5% pure) or silver eagles. Make sure they meet Section 408(m) rules for your IRA.

- Monitor annually. Use apps like Kitco to track values and check statements closely. Watch for purity issues to dodge IRS audits and keep your account safe. Total setup time: 5-10 hours.

Common Pitfalls and Compliance Tips

Managing self-directed IRAs can be tricky. Prohibited transactions, like using your IRA gold personally, violate Section 4975 of the tax code.

Break these IRS rules, and your whole account could get disqualified. You’ll owe taxes on everything plus a 15% penalty – don’t let that happen!

IRS data shows these problems hit about 5% of audited self-directed IRAs. Stay vigilant to avoid joining that group.

To mitigate this risk, it is advisable to engage arm’s-length dealers for all transactions and maintain comprehensive records through IRA custodian-provided logs.

Key considerations:

- Storage rules: Never store IRA metals at home – it’s banned! Use approved spots like the Delaware Depository for coins such as American Eagles or Canadian Maple Leafs to stay compliant.

- Early withdrawals: Pulling money before 59 triggers a 10% penalty on rollover IRAs. Fix this with equal payments via IRS Rule 72(t), calculated from official tables – great for backdoor Roth moves, where you convert traditional IRA funds to Roth after-tax.

- Reporting right: Mess up Form 1099-R, and you might pay taxes twice on inherited or spousal IRAs. Track your cost basis with Form 8606 for correct taxes under Section 408, covering inheritance and backdoor Roth conversions.

Picture this: A 2019 IRS audit nuked a $500,000 gold IRA over a family buy. It led to a $150,000 penalty – same dangers lurk in rollovers and gold IRAs.

The IRS Whistleblower Program has raked in over $6 billion since 2007. It shows how strictly they enforce rules on inherited IRAs and backdoor Roth conversions.