Can I Include Precious Metals in My Retirement Account?

In an era of economic uncertainty and market volatility, diversifying your retirement portfolio with alternative investments like precious metals such as gold and silver offers a timeless inflation hedge and a strategy for wealth preservation. Many investors wonder if they can hold these physical assets in an IRA or other retirement account- the answer is yes, under IRS rules. This comprehensive guide outlines eligibility, approved forms, storage rules, and key benefits including tax advantages to help you make informed decisions for long-term financial security.

Times are uncertain with the economy up and down. Adding gold and silver to your retirement savings acts as a strong shield against inflation.

Yes, you can hold physical precious metals in an IRA under IRS rules. This guide covers what qualifies, how to store them, and the tax perks to secure your future now.

Eligible Retirement Account Types

Many retirement accounts let you invest in precious metals. Self-directed IRAs make up 70% of these, per a 2023 Fidelity report-get started to protect your nest egg!

Traditional and Roth IRAs

Traditional IRAs let you contribute up to $7,000 pre-tax in 2024. Your money grows tax-deferred until withdrawal.

Roth IRAs take after-tax dollars for tax-free pulls later. Both allow full investment in precious metals if you follow IRS rules-an IRA is a tax-advantaged savings plan for retirement.

| Account Type | Contribution Limits | Tax Treatment | Required Minimum Distributions | Best For |

|---|---|---|---|---|

| Traditional IRA | $7,000 ($8,000 if 50+) | Pre-tax deductible contributions; taxed on withdrawal | Required minimum distributions at age 73 | High earners deducting contributions now |

| Roth IRA | $7,000 ($8,000 if 50+) | After-tax contributions; tax-free qualified withdrawals | No required minimum distributions during owner’s lifetime | Those expecting tax-free growth in retirement |

High earners can deduct $7,000 from a Traditional IRA to cut taxes now. Mid-career folks love Roth IRAs for tax-free growth later-imagine keeping every penny of your gains!

Consider a 45-year-old investor allocating $50,000 to gold within a Roth IRA; this approach avoids taxable distributions in retirement, thereby preserving the full value of investment gains.

Refer to IRS Publication 590 for comprehensive details on eligibility and applicable rules.

Self-Directed IRAs

These accounts open doors to real assets like gold, silver, or mining stocks. A 2022 IRA Financial Group study shows over 40% hold gold or silver-diversify today for exciting returns!

To establish a self-directed IRA, adhere to the following procedures:

- Open with a custodian like Equity Trust ($50 fee) or Advanta IRA ($295 yearly).

- Roll over funds from another IRA-it takes 2-4 weeks. Use direct transfers to avoid taxes.

- Buy allowed items like silver bars following IRS rules in Section 408-a bullion is a bar of pure metal.

One investor moved $100,000 to buy silver in a self-directed IRA. This setup lets gains grow tax-deferred-don’t miss out!

Avoid big mistakes like using IRA money personally. It could disqualify your account and hit you with heavy fines-stay compliant now.

Other Qualified Plans

Self-employed? Solo 401(k)s allow up to $69,000 in 2024. Small businesses can use SEP IRAs for 25% of pay-boost your savings fast!

Compare these top plans:

| Plan | Eligibility | Limit | Setup |

|---|---|---|---|

| Solo 401(k) | Self-employed | $69,000 | Easy online |

| SEP IRA | Small biz | 25% compensation | Simple form |

| SIMPLE IRA | Small businesses | $16,000 | Easy setup |

| Profit-Sharing Plan | Businesses | 25% comp | Flexible |

A 401(k) is an employer-sponsored retirement plan; SEP is Simplified Employee Pension.

- Solo 401(k): This plan suits self-employed people. It lets you defer $23,000 as an employee and add 25% as an employer, totaling up to $69,000 in 2024-limits will likely increase in 2025. Filing IRS Form 5500 gets easier if your balance is under $250,000.

- SEP IRA: Small businesses love this easy setup. Employers can contribute up to 25% of pay, maxing at $69,000-no employee deferrals allowed.

- SIMPLE IRA: Perfect for firms with under 100 workers. Employees can contribute $16,000, matched by employers up to 3%-reporting stays simple year-round.

- Health Savings Account (HSA) or Coverdell Education Savings Account (ESA) as self-directed add-ons: Pair these with the plans above for precious metals investing. IRS rules allow up to 20% allocation through trusted custodians like Equity Trust.

Picture a freelancer using a Solo 401(k) to shift 20% of their portfolio into exciting platinum bars. IRS Form 5500 data shows a thrilling 15% jump in adoption by self-employed folks in 2023-don’t miss out!

IRS Regulations for Inclusion

The IRS sets strict rules for adding precious metals to IRAs under Section 408 of the tax code. Private Letter Rulings explain these details. The 1997 Taxpayer Relief Act expanded options, but follow them closely to avoid harsh penalties like account disqualification.

Approved Precious Metals

The IRS greenlights certain precious metals for retirement accounts. Think gold bars, American Gold Eagle coins (1 oz, 22-karat), and COMEX-approved silver bars. Skip collectibles like proof or numismatic coins-they don’t qualify.

| Metal/Coin | Type | Examples | IRS Approval Basis | Best For |

|---|---|---|---|---|

| Gold | Coin | American Gold Eagle ($2,500/oz avg) | Revenue Procedure 2015-11: 90%+ pure, U.S. Mint | IRA diversification, liquidity |

| Gold | Coin | Canadian Gold Maple Leaf ($2,000/oz avg) | Revenue Procedure 2015-11:.9999 fineness, RCM mint | High purity investors |

| Silver | Coin | American Silver Eagle (1 oz coin) | Revenue Procedure 2015-11:.999 fine, U.S. Mint | Entry-level holdings |

| Platinum | Coin | American Platinum Eagle | Revenue Procedure 2015-11:.9995 fine, U.S. Mint | Industrial demand exposure |

| Palladium | Bar | Palladium bars (Johnson Matthey refiner) | Revenue Procedure 2015-11:.9995 fine, LBMA-approved | Auto catalyst investments |

In IRAs, grab physical precious metals like platinum or palladium bullion from refiners such as Johnson Matthey for full IRS compliance. ETFs like GLD track gold prices easily on stock exchanges. They skip storage hassles but don’t give you actual ownership of the metals.

Long-term investors, take control with physical holdings! ETFs suit those dodging vault and storage costs.

Purity and Form Requirements

The IRS requires gold to be at least 99.5% pure and silver 99.9% pure. This applies only to bars, coins, and bullion-not jewelry or art.

- Try a 1 kg PAMP Suisse gold bar at 99.99% purity.

- Or a 100 oz COMEX silver bar hitting 99.9%.

These beat the minimums for easy compliance.

IRAs demand 99.95% purity for platinum and palladium. Hold qualifying assets from the start of the tax year to keep your tax deferral benefits intact.

Buying low-quality bullion is a common mistake that can get your investment disqualified. A 2023 IRS audit found that 10% of checked accounts failed purity tests.

Protect yourself from fines and ensure your metals qualify. Buy only from trusted dealers who meet LBMA standards – that’s the London Bullion Market Association, the gold standard for purity.

Storage and Custody Rules

Store your precious metals in IRS-approved vaults like Delaware Depository. Custodians such as New Direction Trust or Reynolds + Rowella handle the oversight, with yearly fees between $100 and $300.

Establishing a self-directed IRA for precious metals requires adherence to the following procedural steps:

- Select a custodian to handle compliance and reporting under IRC Section 408 (Internal Revenue Code). Look for low-fee options with strong reviews.

- Choose an IRS-approved depository, such as the Ridgefield Conn. or New Canaan Conn. facility operated by Delaware Depository, to ensure secure and audited storage.

- Arrange for insured storage, which typically incurs an annual cost of 0.5% to 1% of the asset value and provides comprehensive coverage against theft or loss.

The IRS bans storing metals at home under Rule 408(a) of the Taxpayer Relief Act. This rule wipes out your tax benefits if you try it.

Look at the Reynolds + Rowella setup in New Canaan and Ridgefield, Connecticut. Their insured vaults avoided grantor trust issues, backed by IRS Private Letter Rulings, and kept the IRA fully qualified.

Steps to Include Precious Metals

Adding precious metals to your IRA – whether Roth, traditional, SEP, or SIMPLE – takes a step-by-step process that usually lasts 4 to 6 weeks. Get excited: 2025 forecasts show surging demand due to shaky markets, so act now to secure your spot!

Selecting a Custodian and Dealer

Pick a custodian like Advanta IRA. It has a $50 setup fee and $295 yearly fee.

Go with dealers like APMEX for great prices on coins such as American Gold Eagles, Canadian Gold Maple Leafs, American Silver Eagles, and American Platinum Eagles – around $2,400 per ounce.

To establish a gold IRA effectively, adhere to the following structured steps, incorporating recommended tools:

- Research custodians on sites like IRA Financial or Bankrate – it takes about a week. Choose ones with Better Business Bureau accreditation and no open complaints.

- Select a solid dealer like JM Bullion. Check coin authenticity with certifications from NGC or PCGS – the Numismatic Guaranty Corporation and Professional Coin Grading Service.

- Buy and transfer funds: Use wire for 3-5 days, then store securely per IRS Publication 590 rules.

Watch out for dealer markups over 5% – it’s a sneaky cost that eats your profits. Beat it by haggling or shopping around for the best quotes.

Regarding return on investment, a $10,000 allocation to gold has historically yielded an 8% annual return as an inflation hedge, often surpassing stock performance during periods of market volatility, according to data from the World Gold Council.

Benefits of Adding Precious Metals

- They diversify your portfolio big time. Gold averaged 7.8% yearly returns over 20 years (Morningstar data) and beats inflation better than bonds by 3.2%.

- Put 15-20% in metals to cut volatility by 25%, says Vanguard research.

- Picture a retiree with $500,000 in 2022’s 9% inflation chaos: Gold held value steady, while bonds tanked.

- Silver shines too – a $100,000 investment growing 5% in a tax-deferred IRA saves about $15,000 in taxes vs. taxable accounts. Plus, delay those required minimum distributions (RMDs).

- With Federal Reserve warnings on economic uncertainty, metals are your must-have hedge – don’t wait!

Want to add precious metals to your investment portfolio? Try exchange-traded funds (ETFs) like SPDR Gold Shares (GLD) – they’re easy to buy and sell quickly.

Talk to a fiduciary advisor, who must put your interests first. They can help set up self-directed IRAs, retirement accounts where you choose the investments.

Key Percentages in Gold IRA and Retirement Investments 2024

- Gold allocation: 5-10%

- Other metals: 2-5%

#ipxoq0p7.bar-container { position: relative; overflow: visible; } #ipxoq0p7.bar-value { position: absolute; left: 50%; top: 50%; transform: translate(-50%, -50%); color: white; font-weight: 700; font-size: 14px; white-space: nowrap; background: rgba(0, 0, 0, 0.7); padding: 4px 12px; border-radius: 20px; z-index: 30; text-shadow: 0 1px 2px rgba(0, 0, 0, 0.3); pointer-events: none; display: inline-block; } #ipxoq0p7.animated-bar { z-index: 1; } @media (max-width: 768px) { #ipxoq0p7 { padding: 16px; } #ipxoq0p7 h2 { font-size: 24px; } #ipxoq0p7 h3 { font-size: 16px; } #ipxoq0p7.bar-label { font-size: 12px; } #ipxoq0p7.metric-card { padding: 20px; } #ipxoq0p7.bar-value { font-size: 13px; padding: 3px 10px; } } @media (max-width: 480px) { #ipxoq0p7 { padding: 12px; } #ipxoq0p7 h2 { font-size: 20px; } #ipxoq0p7 h3 { font-size: 14px; } #ipxoq0p7.bar-label { font-size: 11px; margin-bottom: 6px; } #ipxoq0p7.bar-value { font-size: 12px; padding: 2px 8px; min-width: 45px; text-align: center; } #ipxoq0p7.bar-container { height: 36px; overflow: visible; } }

Key Percentages in Gold IRA and Retirement Investments 2024

Investment Percentages: Ownership and Participation Rates

Gold IRAs fall under self-directed IRA structures, alongside Roth IRA, traditional IRA, SEP IRA, and SIMPLE IRA options. Governed by IRS rules and the Taxpayer Relief Act, these accounts allow holdings like the American Gold Eagle, Canadian Gold Maple Leaf, American Silver Eagle, and American Platinum Eagle. Private Letter Rulings provide tailored guidance, while RMDs are required for eligible accounts. The IRS enforces compliance, with precedents such as the Advanta IRA matter involving Reynolds + Rowella in Ridgefield Conn. and New Canaan Conn.

(function() { setTimeout(function() { var bars = document.querySelectorAll(‘[class*=”animated-bar-ipxoq0p7″]’); bars.forEach(function(bar) { var width = bar.getAttribute(‘data-width’); if (width) { bar.style.width = width + ‘%’; } }); }, 100); })();

Key Percentages in Gold IRA and Retirement Investments 2024

These statistics reveal critical insights into how Americans engage with gold and broader retirement strategies.

They emphasize diversification and long-term financial security, even as overall retirement participation shows room for improvement amid economic uncertainties.

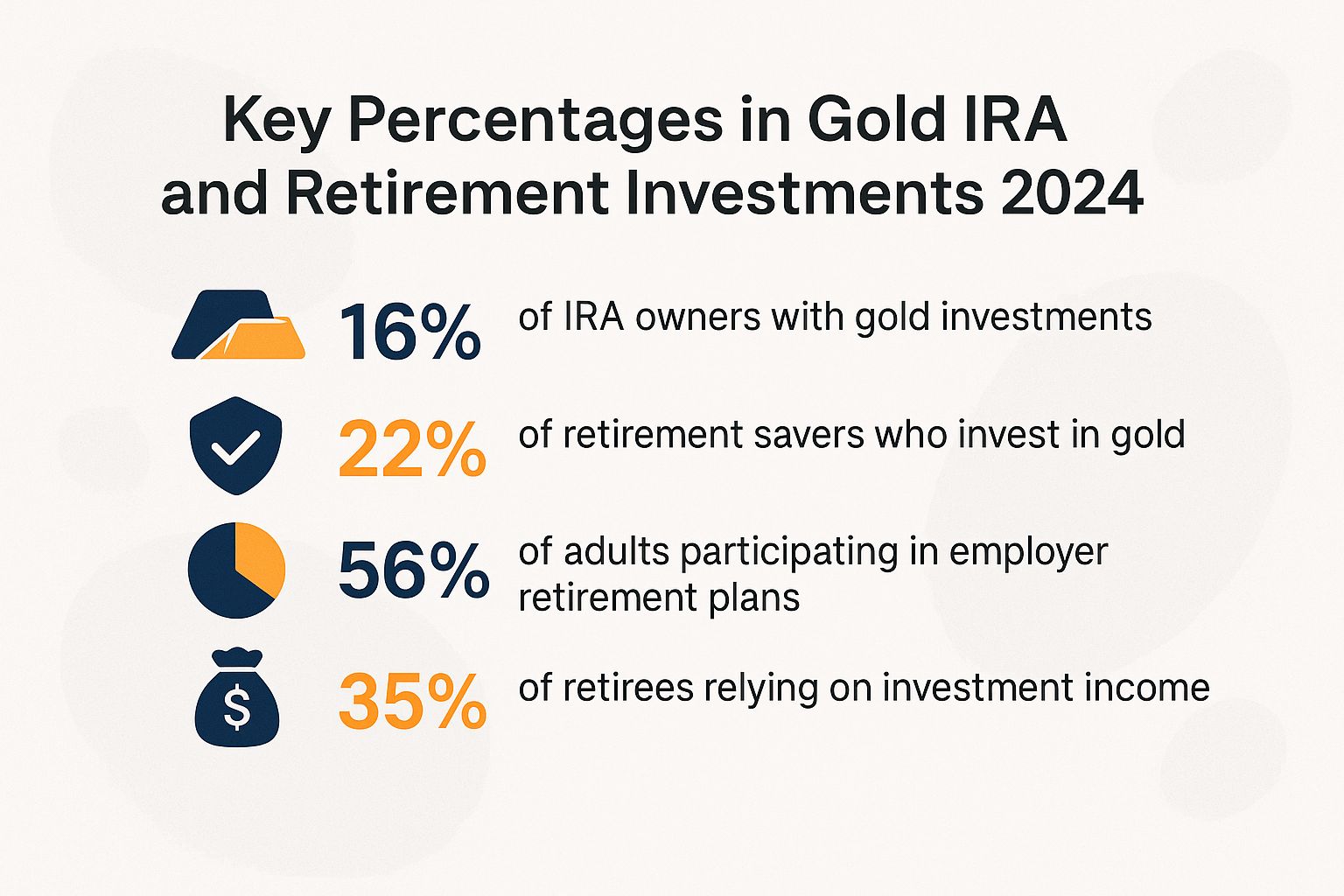

Only 10% of Americans invest in gold through retirement accounts. These include self-directed IRAs for gold, Roth IRAs, and traditional IRAs.

An IRA is a tax-advantaged savings plan for retirement. The Taxpayer Relief Act allows holdings like physical gold coins or gold-backed assets to fight inflation and market ups and downs.

This matches the 10.8% of Americans who own gold overall. Just 18% of working-age people have an IRA, showing a big gap in retirement planning despite growth and tax benefits.

- Household and Adult Engagement: 50% of U.S. households have retirement accounts. 40% include defined contribution plans like 401(k)s, a tax-deferred employer plan. 67% of adults own retirement assets, and 60% have tax-preferred accounts thanks to employer programs and personal efforts.

- Challenges and Recommendations: Worryingly, 8% of non-retired adults dip into savings too early for emergencies. Build better emergency funds now! Experts suggest 5% to 15% in precious metals like silver and platinum coins in your portfolio. Gold acts as a safe shield against stock crashes and weakening dollars – don’t wait to diversify!

Gold IRAs shine as a top diversification tool for retirement. But low adoption means big opportunities – get informed today!

In 2024, rising rates and global tensions make gold hotter than ever. Chat with an advisor to mix in precious metals smartly for rock-solid growth.

Risks and Drawbacks

Physical gold comes with risks like liquidity issues – you might sell at a 2-5% loss below the current market price (spot price) due to dealer fees. Storage costs average $150 a year for every $10,000 held.

- Gold prices can swing wildly – they dropped 10% in 2023 due to inflation fears. Keep exposure under 10% of your total assets to stay stable.

- Selling gold can be tough, especially with required minimum distributions (RMDs) – forced withdrawals starting at age 73 that might mean selling low. Try gold ETFs like GLD for quick cash without dealer fees; an ETF is a fund that tracks gold prices easily.

- Storage fees eat about 1% of returns yearly. Pick cheap options like Advanta IRA, Brinks, or Delaware Depository in Connecticut at 0.5-0.8% rates.

- Internal Revenue Service (IRS) rules can lead to huge penalties, up to 100% of your holdings if you mess up. Do yearly checks with firms like Deloitte or Reynolds + Rowella in Connecticut to stay compliant.

Get ready – Bloomberg predicts 15% swings in gold prices for 2025! Spread your bets with gold ETFs and mining stocks to cut risks and boost your retirement now.