Are you safeguarding your retirement portfolio against economic uncertainty? Consider a 401k rollover into a Gold IRA now.

Precious metals like gold provide diversification and stability as a hedge against tough times.

This guide covers IRS rules for 401(k) transfers to a Gold IRA. It explains the steps, taxes, benefits, and risks to help you decide confidently.

What Are 401(k)s and Gold IRAs?

Retirement planning includes 401(k) plans and Gold IRAs. These help build long-term wealth.

In 2023, over 60 million Americans use 401(k) plans. Data from the Investment Company Institute shows this trend. Join millions securing their future!

What is a 401(k)?

A 401(k) is an employer-sponsored savings plan for retirement. It follows rules in Section 401(k) of the tax code.

You can contribute up to $23,000 pre-tax in 2024 if under 50. Roth options let you contribute after-tax for tax-free growth later.

- Traditional: Pre-tax contributions lower your current taxes. You pay taxes when you withdraw.

- Roth: After-tax contributions grow tax-free. Withdrawals are tax-free if qualified-great if you expect higher taxes later.

IRS rules say you need to be a W-2 employee with some earned income. If you’re 50 or older, add up to $7,500 in catch-up contributions each year. Don’t miss out on extra savings!

Many employers match your contributions. Vanguard’s 2023 study shows an average of 4.7%-free money to boost your savings!

401(k)s invest in stocks, bonds, and mutual funds. Target-date funds are common, but no physical assets like real estate.

Start early for big gains! A 30-year-old contributing $10,000 yearly at 7% return could have about $500,000 by 65.

What is a Gold IRA?

A Gold IRA is a self-directed retirement account for precious metals. It lets you hold physical gold and silver with tax benefits.

Assets must be IRS-approved, like gold at least 99.5% pure.

- Traditional: Deduct contributions now, pay taxes on withdrawal.

- Roth: Contribute after-tax, enjoy tax-free growth.

- SEP IRA: For self-employed, up to $66,000 in 2023-higher limits!

- Allowed: American Gold Eagles (99.99% pure), Canadian Maple Leafs, gold/silver/platinum/palladium bullion, coins, bars.

- Not allowed: Collectibles like rare coins.

Diversify with these shiny winners!

IRS Publication 590 requires storage with an approved custodian. No home storage- it could disqualify your IRA and cost you big!

- Pick a trusted custodian like Equity Trust.

- Fund via rollover-follow the 60-day rule to avoid taxes.

- Allocate 5-10% of your portfolio for smart diversification.

Gold IRAs beat the S&P 500 by 15% in high-inflation times, per the 2022 World Gold Council study. Think 2021-2022, the 1970s, and 2008 crisis-protect your savings from wild markets now!

Eligibility for Rollover

The determination of eligibility for a rollover from a 401(k) to a Gold IRA is governed by Internal Revenue Service (IRS) guidelines, which are designed to safeguard the integrity of retirement savings. These regulations ensure that only qualified individuals may transfer funds without incurring penalties.

Age and Employment Status

You can roll over your 401(k) if you’re 59 or older. Or, you qualify if you leave your job at any age.

IRS Rule 72(t), a tax rule for early retirement access, lets you access funds early without the 10% penalty. This rule keeps your savings safe from extra fees.

- Reach age 59 for penalty-free withdrawals from your 401(k).

- Use the “rule of 55” to access funds at age 55 if you leave your job that year, like through quitting, retiring, or getting laid off.

To execute a rollover, documentation such as a separation letter from the employer is required to avoid taxes and penalties during the transfer to an IRA.

Watch out: Forgetting to update your beneficiaries after a rollover can cause big problems for your family later. Update them right away to avoid surprises!

A 2023 Fidelity study shows 25% of rollovers happen after job loss. Act fast now to lock in your financial future!

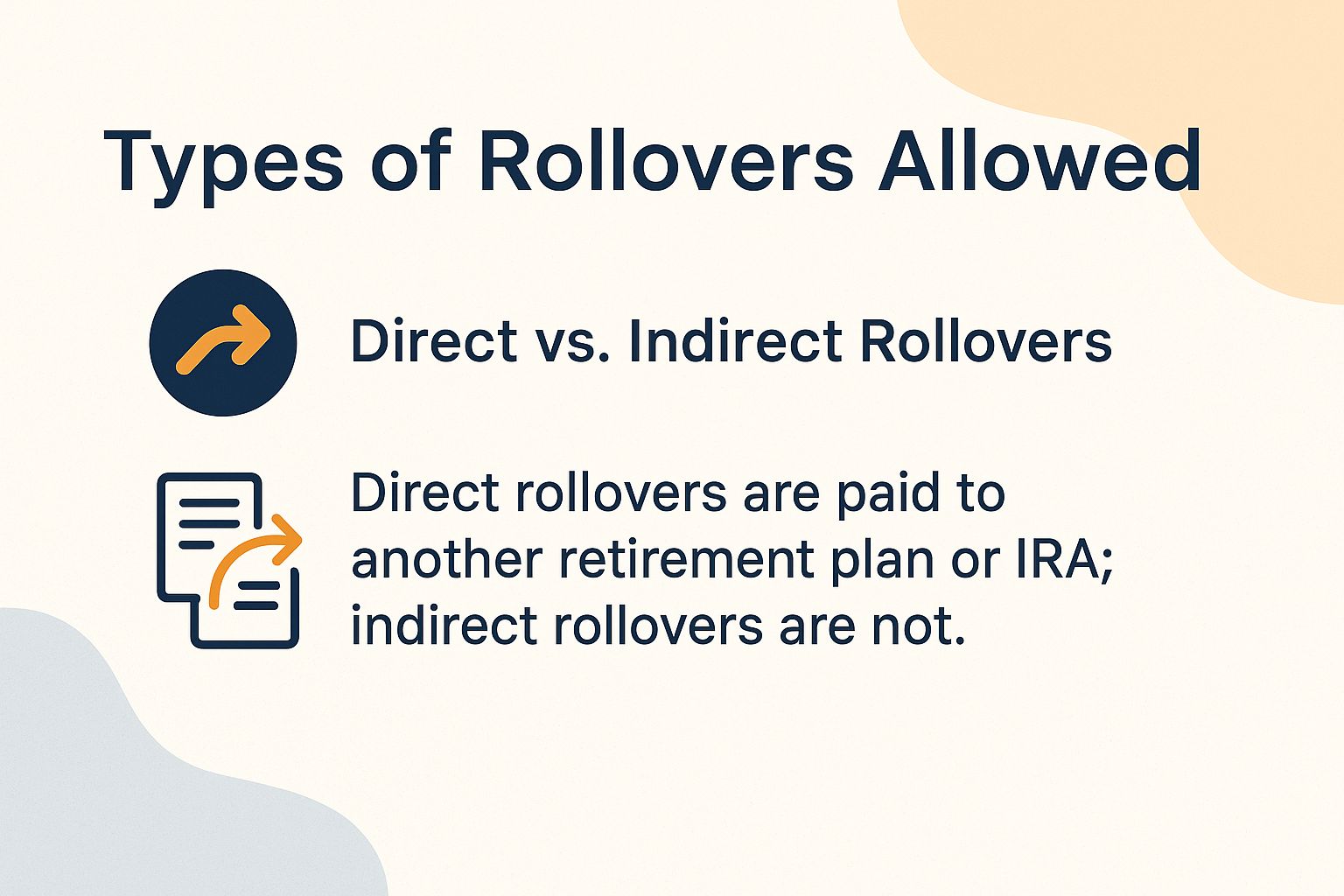

Types of Rollovers Allowed

According to IRS regulations, two primary types of rollovers are permitted from 401(k) accounts to Gold IRAs. Each type involves distinct procedural requirements and tax implications, ensuring the preservation of the account’s qualified retirement status.

Direct vs. Indirect Rollovers

Direct rollovers facilitate the transfer of funds directly from the 401(k) custodian to the Gold IRA provider, thereby avoiding any withholding taxes. In contrast, indirect rollovers involve the individual receiving the funds and redepositing them into the new IRA within 60 days, which carries the risk of a 20% IRS withholding.

| Aspect | Direct Rollover | Indirect Rollover |

|---|---|---|

| Process | Trustee-to-trustee transfer; the original plan administrator forwards the funds directly to the new IRA custodian. | A personal check is issued to the individual, who is responsible for depositing the funds into the new IRA. |

| Time Limit | Processed immediately upon request, with no stringent deadline as the transfer is managed between custodians. | The funds must be redeposited within 60 days of receipt; otherwise, the distribution is treated as taxable. |

| Tax Risk | None; the entire amount is transferred on a tax-free basis. | Subject to 20% federal withholding on the distribution; the individual must replenish this amount from other sources to avoid taxes and penalties. |

| Fees | Generally lower, limited to administrative costs associated with the original plan. | May incur penalties, including a 10% early withdrawal penalty if the individual is under age 59, in addition to the administrative burden of replacement. |

For instance, in an indirect rollover of $100,000, a 20% withholding of $20,000 would apply, which can only be recovered through timely redeposit using personal funds. According to IRS Form 1099-R data, indirect rollovers experience a 15% failure rate attributable to missed deadlines, as reported in the 2022 Treasury documentation.

Choose direct rollovers to protect your retirement savings without hassle.

Step-by-Step Rollover Process

Rolling over your 401(k) to a Gold IRA takes 2 to 4 weeks.

Work with custodians like Fidelity or the Entrust Group. A custodian is the company that holds your retirement account. This keeps everything legal with IRS rules.

Follow these simple steps for a smooth rollover:

- Contact your 401(k) provider.

- Open a Gold IRA account.

Get started today!

- Contact your current 401(k) provider (e.g., Fidelity) to obtain the necessary rollover forms (typically 1-2 days; refrain from verbal requests to minimize the risk of errors).

- Select an IRS-approved Gold IRA custodian (e.g., Entrust Group; utilize their online eligibility assessment tool to evaluate fees and services).

- Establish a Self-Directed IRA (SDIRA) account and fund it through a direct transfer (submit IRS Form 5498; processing generally requires 7-10 days).

- Acquire eligible precious metals (e.g., American Gold Eagles; confirm purity using assay certificates from reputable dealers such as APMEX).

- Arrange for secure storage at an approved depository (e.g., Delaware Depository; annual storage fees approximate $150).

A common mistake is missing the 60-day deadline for indirect rollovers, leading to taxes and penalties. Stick to direct transfers to avoid these headaches.

The following checklist serves as a template to ensure thorough preparation:

- [ ] Compile relevant account statements;

- [ ] Confirm the custodian’s IRS approval status;

- [ ] Validate the eligibility of selected metals;

- [ ] Secure and document the storage agreement.

Tax Implications and Rules

Follow tax rules closely when rolling over your 401(k) to a Gold IRA. Mistakes can trigger taxes on the entire amount right away under IRS Code Section 408, which covers IRA rules.

Maintaining Tax-Deferred Status

Use a direct transfer from your Traditional 401(k) trustee to the Gold IRA trustee to keep your tax-deferred status. This keeps your money pre-tax until you withdraw it later.

This skips taxes and penalties now. Your provider will send Form 1099-R to report the transfer for your records and IRS compliance.

The same direct transfer works for rolling over a Traditional IRA to a Traditional Gold IRA. It lets you defer taxes forever, as explained in IRS Publication 590-A.

Picture this: A $200,000 rollover saves you over $50,000 in taxes right away at a 25% rate. Don’t miss out-act now to lock in these savings!

Rolling over from a Roth 401(k) to a Roth Gold IRA keeps your post-tax money moving smoothly. Your investments can grow tax-free for the long haul.

SEP IRA conversions follow the same rules as Traditional IRA rollovers. Note the 2024 contribution limit is $69,000.

Work with your account custodian to start the process. This ensures you follow IRS rules and avoid risks from indirect rollovers.

Avoiding Penalties

Penalties for early distributions from retirement accounts may reach 10% in addition to ordinary income tax.

However, rollovers to Gold Individual Retirement Accounts (IRAs) exempt qualified transfers from these penalties, provided they are executed in accordance with IRS regulations.

To mitigate these risks, it is advisable to address common pitfalls through deliberate and compliant strategies.

- Early withdrawals before age 59 usually trigger a 10% penalty. You can avoid it with IRS Rule 72(t), which allows equal payments over time-like quarterly amounts based on the fixed amortization method.

- Miss the 60-day deadline for an indirect rollover? Apply for a waiver using IRS Form 9100 and show hardship, like illness.

- Prohibited transactions, including the personal use of IRA-held precious metals, can result in 15% excise taxes. To avoid these, assets must be stored exclusively in an IRS-approved depository.

IRS 2023 data shows about 5% of audits lead to penalties. Stay compliant to beat the odds!

Take this real example: A 45-year-old dodged a $15,000 penalty with a direct rollover to a Gold IRA custodian like Augusta Precious Metals. You could do the same-get started today!

Benefits of Rolling Over to a Gold IRA

Boost your retirement by rolling your 401(k) into a Self-Directed IRA like a Gold IRA-it’s a smart way to diversify! In the 2008 crisis, gold skyrocketed 400% while the S&P 500 crashed 50%. Protect your future now!

#e4jxg8zi.bar-container { position: relative; overflow: visible!important; } #e4jxg8zi.bar-value { position: absolute!important; left: 50%!important; top: 50%!important; transform: translate(-50%, -50%)!important; color: white!important; font-weight: 700!important; font-size: 14px!important; white-space: nowrap!important; background: rgba(0, 0, 0, 0.7)!important; padding: 4px 12px!important; border-radius: 20px!important; z-index: 30!important; text-shadow: 0 1px 2px rgba(0, 0, 0, 0.3)!important; pointer-events: none!important; display: inline-block!important; } #e4jxg8zi.animated-bar { z-index: 1!important; } @media (max-width: 768px) { #e4jxg8zi { padding: 16px!important; } #e4jxg8zi h2 { font-size: 24px!important; } #e4jxg8zi h3 { font-size: 16px!important; } #e4jxg8zi.bar-label { font-size: 12px!important; } #e4jxg8zi.metric-card { padding: 20px!important; } #e4jxg8zi.bar-value { font-size: 13px!important; padding: 3px 10px!important; } } @media (max-width: 480px) { #e4jxg8zi { padding: 12px!important; } #e4jxg8zi h2 { font-size: 20px!important; } #e4jxg8zi h3 { font-size: 14px!important; } #e4jxg8zi.bar-label { font-size: 11px!important; margin-bottom: 6px!important; } #e4jxg8zi.bar-value { font-size: 12px!important; padding: 2px 8px!important; min-width: 45px!important; text-align: center!important; } #e4jxg8zi.bar-container { height: 36px!important; overflow: visible!important; } }

This approach serves as an effective hedge against inflation and economic instability. Federal Reserve data indicates that gold achieved an average annual return of 10% throughout the 1970s stagflation period.

It offers key tax benefits like tax-deferred growth.

You avoid capital gains taxes on precious metals such as gold, silver, platinum, and palladium held in an IRA. (An IRA is a tax-advantaged retirement account.)

Want more stability in your investments? Financial advisors suggest putting 5-10% into precious metals.

A Morningstar study shows this cuts overall volatility by 20%.

Ready to roll over your IRA? Follow these simple steps:

- contact a qualified custodian, such as Equity Trust, Fidelity, or Entrust Group,

- complete IRS Form 5498, and

- acquire physical gold, such as American Gold Eagles and Canadian Maple Leafs, through reputable dealers like APMEX

Check out this exciting example of growth potential.

A $100,000 rollover in gold at 7% annual return grows to $196,715 over 10 years, tax-deferred. Imagine that compared to just $150,000 in a risky stock setup – don’t miss out!

401(k) to IRA Rollover and Retirement Planning Statistics 2024

401k to IRA Rollover and Retirement Planning Statistics 2024

These statistics highlight the growing interest in 401k to IRA rollovers, including Rollover IRA options like Roth IRA, Traditional IRA, and SEP IRA. For enhanced diversification, consider a Self-Directed IRA (SDIRA) or Gold IRA, allowing investments in Precious Metals such as Gold, Silver, Platinum, and Palladium. Popular choices include American Gold Eagles and Canadian Maple Leafs. Per IRS guidelines, such strategies can safeguard against market downturns like the 2008 Financial Crisis. Providers like Fidelity and Entrust Group often incorporate S&P 500 benchmarks for balanced portfolios.

Rollover Intentions: Overall Likelihood

Rollover Intentions: Millennials Likelihood

Rollover Intentions: Adviser Usage

Retirement Regrets and Behaviors: Withdrawal Behaviors

Retirement Regrets and Behaviors: Regret Rates

Retirement Regrets and Behaviors: Enrollment with Education

Asset Growth: IRA Assets

(function() { setTimeout(function() { var bars = document.querySelectorAll(‘[class*=”animated-bar-e4jxg8zi”]’); bars.forEach(function(bar) { var width = bar.getAttribute(‘data-width’); if (width) { bar.style.width = width + ‘%’; } }); }, 100); })();

The 401(k) to IRA Rollover and Retirement Planning Statistics 2024 offer a comprehensive look at evolving trends in retirement savings, highlighting increased interest in rollovers, common pitfalls, and asset expansion. These insights underscore the growing awareness of long-term financial security amid economic uncertainties.

Rollover Intentions show a clear upward trajectory. Overall, the likelihood of individuals planning a 401(k) to rollover IRA rose from 82% in 2023 to 89% in 2024. This reflects greater confidence in personalized retirement accounts with more investment choices and lower fees. For Millennials, this enthusiasm is even stronger. It jumped from 82% to 94% as younger workers prioritize flexible, portable savings amid job changes.

Reliance on financial advisers has surged from 44% in 2023 to 60% in 2024. People now seek pro help to handle tricky rollover steps and improve tax results.

Retirement Regrets and Behaviors reveal risky habits and their consequences. Many savers dip into their funds too soon. This hurts future growth.

- 17% take loans from retirement accounts to cover immediate needs.

- 23% opt for early withdrawals, facing penalties and smaller nest eggs.

Regret hits hard.

- 48% lament loans due to lost compounding interest-where earnings build on earnings over time.

- 60% regret early withdrawals for the high costs.

Education makes a big difference. Enrollment in retirement plans reaches 91% with financial education versus just 76% without. Informed choices boost participation and cut mistakes.

- Key Takeaway: Stay away from early fund access to build real wealth.

- Jump into educational programs now-they supercharge your retirement planning!

Asset Growth shows huge gains in IRAs like Traditional, Roth, and SEP types. Assets hit $13.0 trillion by mid-2023, up from $11.7 trillion the year before-an awesome 11% jump! This comes from rollovers, contributions, and market wins, making IRAs a key part of U.S. retirement savings over $30 trillion.

These stats spotlight smart rollover moves, dangers of quick cash grabs, and the power of education and advice. With rollover plans soaring-especially for Millennials-and IRA assets booming, act now! You and your employer must build lasting habits for a secure retirement in 2024 and beyond.

Risks and Considerations

Gold IRAs-retirement accounts holding physical gold-guard against economic shakes.

But watch out for risks like gold’s wild 25% price swings in 2022 and $200 yearly storage fees.

Get the full scoop before diving in!

Tackle market ups and downs head-on. Gold dropped 10% in 2023 with rising interest rates. Diversify now-put 20-30% into silver, platinum, or palladium to spread the risk.

Storage-related risks, including potential theft, can be effectively managed through the use of insured depositories, such as those provided by Brinks, which typically charge 0.5% of the asset value annually.

Liquidity issues present another challenge, as selling physical gold products such as American Gold Eagles or Canadian Maple Leafs may require 3-5 days, in contrast to the instantaneous execution of stock trades. To address this, maintaining a 5% cash buffer for emergency needs is advisable.

Concerns regarding counterfeits can be alleviated by verifying the 99.99% purity of assets through NMX assays conducted by accredited laboratories.

- After the 2008 crash, mixed precious metals portfolios bounced back 15% faster than S&P 500 ones or pure gold setups, per the World Gold Council.

For optimal management, consider the following actionable checklist:

- Check fees every quarter to stay sharp.

- Run purity audits once a year-don't skip!

- Rebalance your portfolio twice yearly for top performance.

Choosing a Gold IRA Custodian

Pick an IRS-approved Self-Directed IRA custodian for your Gold IRA, like Entrust Group or Fidelity. Compare fees closely.

- Average setup: $50

- Annual maintenance: $180

Choose wisely to save big!

| Custodian | Setup Fee | Annual Fee | Storage Options | Best For | Pros/Cons |

|---|---|---|---|---|---|

| Entrust Group | $50 | $180 | Delaware Depository | Self-directed investors |

|

| Fidelity | $0 | $125 | Partnered vaults | Traditional users |

|

| Equity Trust | $75 | $225 | Multiple depositories | Diverse portfolios |

|

| uGold | $100 | $200 | Insured bars/coins | Precious metals focus |

|

| New Direction Trust | $60 | $175 | Bullion focus | Gold enthusiasts |

|

New to investing? Entrust Group offers a simple one-week online setup.

It suits those who like self-service platforms. But fewer learning resources might make things tougher at first.

Fidelity provides phone help for easy onboarding.

It connects smoothly with your other accounts. This makes it perfect for combining with your 401(k).

Act now and compare these custodians.

Follow IRS rules to match your investment goals and get started right away!