Global debt has exploded past $300 trillion. Gold, the timeless safe haven, shields against inflation and economic storms.

Discover the gold standard’s history, the switch to fiat cash, and debt-driven economies. See how gold battles rising sovereign debt-perfect for diversifying your portfolio now!

The Historical Role of Gold in Monetary Systems

Gold has been the backbone of money systems for centuries. It started in ancient times with gold mining and lasted until the 20th-century gold standard.

Back then, you could swap your currency for gold at a fixed rate. For example, the U.S. set it at $20.67 per ounce in 1900, creating stable, trustworthy money.

The Gold Standard Era

The gold standard kicked off in the 1870s in places like Britain and the U.S. It tied money to gold, keeping trade steady and inflation under 1% yearly from 1870 to 1914.

This setup stopped wild price swings and money losing value fast. Studies from the National Bureau of Economic Research back this up.

Currencies could turn into gold at set prices, helping balance global payments with gold and reserve flows.

Britain started in 1821, boosting trade with clear prices. The U.S. made it law in 1900, keeping gold prices steady until 1933.

The gold standard kept inflation in check and trade reliable. But it limited how governments could tweak money during booms or busts. A timeline of significant developments is outlined below:

- 1870s: Widespread adoption

- 1914: Suspension due to World War I

- 1925: Partial reinstatement

- 1933: Onset of abandonment

Economist Milton Friedman, in his book ‘Money Mischief,’ shows how the gold standard’s stiff rules worsened the Great Depression. This pushed the world toward flexible fiat money we use today.

Abandonment of the Gold Standard

In 1944, the Bretton Woods system tied world currencies to the U.S. dollar. The dollar itself was backed by gold at $35 per ounce- a fresh start after chaos.

But it all fell apart in 1971. President Nixon ended dollar-to-gold swaps, kicking off floating exchange rates that fluctuate with markets.

In 1933, amid the Great Depression, President Roosevelt slashed the dollar’s value by 40% against gold. He raised the price from $20.67 to $35 per ounce via the Gold Reserve Act.

This aimed to boost exports and prices at home. Yet it exposed flaws in fixed rates, like risks to credit and defaults-gold links crumbled globally by 1936.

World War II ramped up the pressure with geopolitics in flux. It wrecked European economies and crowned the U.S. as the top economic power.

By 1944, the U.S. held about two-thirds of global gold reserves-around 20,000 tons at Fort Knox. Federal records note this, sparking endless audit demands today.

The 1944 Bretton Woods Conference at New Hampshire’s Mount Washington Hotel fought to prevent more depressions. It created the IMF and World Bank to stabilize the world economy-don’t miss how this shapes your investments today!

Representatives from 44 nations agreed to peg their currencies to the U.S. dollar, with the United States pledging to redeem dollars for gold at the established fixed rate.

As outlined in the IMF’s founding documents, the organization’s objectives include “to promote international monetary cooperation… and to facilitate the expansion and balanced growth of international trade and the global economy.”

After World War II, the system faced huge pressure.

Countries rebuilt fast, and wars cost a lot.

The U.S. ran ongoing trade deficits. It funded the Marshall Plan and Korean War, leading to too many dollars worldwide.

U.S. gold reserves peaked at 20,000 tons in 1950. They dropped later as other countries demanded gold and banks sold it.

Europe rebuilt quickly after the war. These countries collected dollars but doubted the U.S. would always swap them for gold.

Tensions grew in the 1960s. The Vietnam War and Johnson’s Great Society programs boosted U.S. spending sky-high.

Gold outflows intensified, reducing reserves to 8,000 tons by 1971, according to World Gold Council data.

Get ready for a game-changer! On August 15, 1971, President Nixon shocked the world on TV by pausing the dollar-to-gold swap.

He declared: “I have directed the Secretary of the Treasury to defend the dollar against speculators. We must safeguard America’s trading strength!”

This announcement, known as the “Nixon Shock,” effectively dismantled the Bretton Woods system.

It prompted the Smithsonian Agreement later that year, which attempted a short-lived return to fixed exchange rates, but this effort ultimately succumbed to speculative pressures.

The fallout hit hard and fast worldwide.

- In the U.S., prices jumped 5.7% in 1971, up from 4.3% the year before (Bureau of Labor Statistics). This fueled 1970s stagflation-high inflation mixed with slow growth.

- Globally, floating rates made currencies swing wildly.

Before 1971, bond yields stayed steady. 10-year Treasuries averaged 4.2% in the 1960s, with low ups and downs.

- After 1971, things got wild: Yields hit 7.5% on average in the 1970s.

- Volatility tripled to 1.8% (Federal Reserve Economic Data).

Central banks gained more freedom to act. But it brought wild uncertainty and economic rollercoasters-like the dollar dropping 20% versus the yen by 1973.

Today, exciting options like Bitcoin and cryptocurrency are rising fast. They use blockchain-a secure digital ledger-to offer stable ‘sound money.’ Central banks eye digital currencies and CBDCs too.

IMF records from 1973 observed that “the par value system has broken down,” marking the shift to the contemporary fiat currency regime and the establishment of the petrodollar system.

While exchange rate volatility endures, this framework affords central banks enhanced flexibility in conducting monetary policy.

Rise of Fiat Currency and Debt Monetization

After ditching gold in 1971, fiat money-currency backed only by government promise-freed central banks like the Fed. They could print more cash through debt monetization, which means buying government debt to boost the economy.

The U.S. money supply (M2) exploded from $600 billion in 1971 to $21 trillion in 2023 (Federal Reserve data).

Governments buy Treasury bonds with this money. This floods the economy with cash, called liquidity.

Take quantitative easing (QE)-it’s like dropping cash from helicopters. After the 2008 crisis, the Fed bought $4.5 trillion in assets to cut rates and spark growth (Federal Reserve). But it risked moral hazard, where people take big risks expecting bailouts.

The European Central Bank (ECB) bought EUR2.6 trillion in assets since 2015. This money growth often leads to higher prices.

Look at the 1970s stagflation-when prices rose fast and the economy stalled. The U.S. Consumer Price Index hit 13.5% as money supply grew quickly. Charts show the M2 money supply line shooting up before inflation peaks. Governments gain from this through seigniorage, which is profit from printing money.

Austrian economists disagree with Keynesian ideas. Thinkers like

- Friedrich Hayek, in his 1976 book Denationalisation of Money,

- Ron Paul,

- Peter Schiff, and

- Jim Rickards

slam these policies. They say it slowly destroys money’s value and leads to bad investments, called malinvestment.

Gold is a top pick for mixing up your investments today. You can buy physical gold bars, gold ETFs, or trade futures.

In futures, the spot price is today’s value. Contango means future prices are higher; backwardation means lower-both shape your trades. Gold mines face issues like supply delays, higher costs, all-in sustaining costs (total expenses to keep mining), ore quality, and refining steps. Don’t miss out-gold could protect your wealth!

Understanding Modern Government Debt

U.S. government debt hit $34 trillion in 2024, per the US Treasury. It grows because spending outpaces income by $1.7 trillion each year in expansionary policies.

Key Drivers of Debt Accumulation

Big spending on Social Security and Medicare drives up U.S. debt. The Congressional Budget Office says these programs will add $50 trillion to deficits over 30 years, sparking worries about the debt ceiling. This could spell trouble-act now to understand the risks!

- Military spending: Military spending hit $877 billion in 2023, about 15% of the budget (Stockholm International Peace Research Institute). It’s often seen as a way to boost the economy, but closing bases could cut costs by 5-10% safely, like after the Cold War.

- Demographic shifts: An aging population is expected to double pension costs by 2050 (United Nations and World Bank estimates), thereby increasing the debt-to-GDP ratio by 20%. Reforms, including adjustments to retirement ages as recommended by the International Monetary Fund, have proven effective in nations like Sweden.

- Low productivity growth: Annual productivity growth has averaged 1.5%, compared to the historical norm of 2.5% (Bureau of Labor Statistics data), which diminishes revenue streams. Strategic investments in artificial intelligence and education could enhance productivity by 0.5%, according to CBO analyses.

- Tax cuts: The 2017 Tax Cuts added $1.9 trillion to debt (Joint Committee on Taxation). Modern Monetary Theory says deficits are okay if prices stay low. But Ricardian equivalence means people save the cuts expecting higher taxes later. Bringing back rules for the rich could save $500 billion in 10 years, like in Clinton’s time when debt-to-GDP fell from 64% to 55%. Time to rethink-your savings are at stake!

- Debt-to-GDP ratio: Now 120%, could hit 180% by 2053 (CBO). This measures debt against economy size.

- Persistent deficit spending: Governments keep spending more than they earn, piling on debt year after year.

- Geopolitical tensions: Trade wars and sanctions cause capital flight and stress the global economy.

- Impacts on funds and savings: Sovereign wealth funds, pension funds, and retirement savings are at risk, threatening wealth preservation.

- Rising default risk: Higher chance of not paying debts, leading to credit rating downgrades.

- Policy debates: Arguments over austerity, Keynesian economics, and Modern Monetary Theory create crowding out and moral hazard, challenging Ricardian equivalence.

- Conspiracy theories: Doubts about gold reserves at Fort Knox, calls to end the Fed, and interest in returning to the gold standard.

Why Gold Shines When Government Debt Soars: The Surprising Connection

The Nixon shock hit in 1971. It ended the Bretton Woods system, where dollars could be swapped for gold, and kicked off huge growth in government debt.

Gold prices often drop when debt rises. During the 2011 U.S. debt crisis, gold surged 25% while 10-year Treasury yields spiked to 3.7%.

| Asset | Behavior with Rising Debt Fears | Example | Performance Data |

|---|---|---|---|

| Gold | Rises as a safe haven. Debt scares weaken trust in paper money, driving up gold demand. | 2008 financial crisis: +30% price gain (World Gold Council) | +400% since 2000 (Kitco); inverse correlation of -0.65 with debt levels (Bloomberg, 2000-2023) |

| Treasury bonds | Value drops as yields climb. This signals bigger risks ahead. | 2011 Italian bonds: yields reached 7% | Yields rose sharply as gold prices surged; bonds experienced principal value losses |

Debt crises shake trust in everyday money. World Gold Council reports back this up.

Thinkers from the Austrian school of economics blast the Federal Reserve. They say it fuels endless debt-Ron Paul pushes to ‘end the Fed,’ while Peter Schiff and Jim Rickards warn of coming trouble.

Ray Dalio advises 5-10% of your investments in gold. It shields against debt dangers, and mix in Treasury bonds for smart spread-out protection.

Bitcoin draws fans as a fresh hedge too. It stands apart from controlled options like Central Bank Digital Currencies (CBDCs), which governments back.

Jump into action today! Track yield jumps on Bloomberg terminals and snag gold ETFs at peak moments to ride the wave.

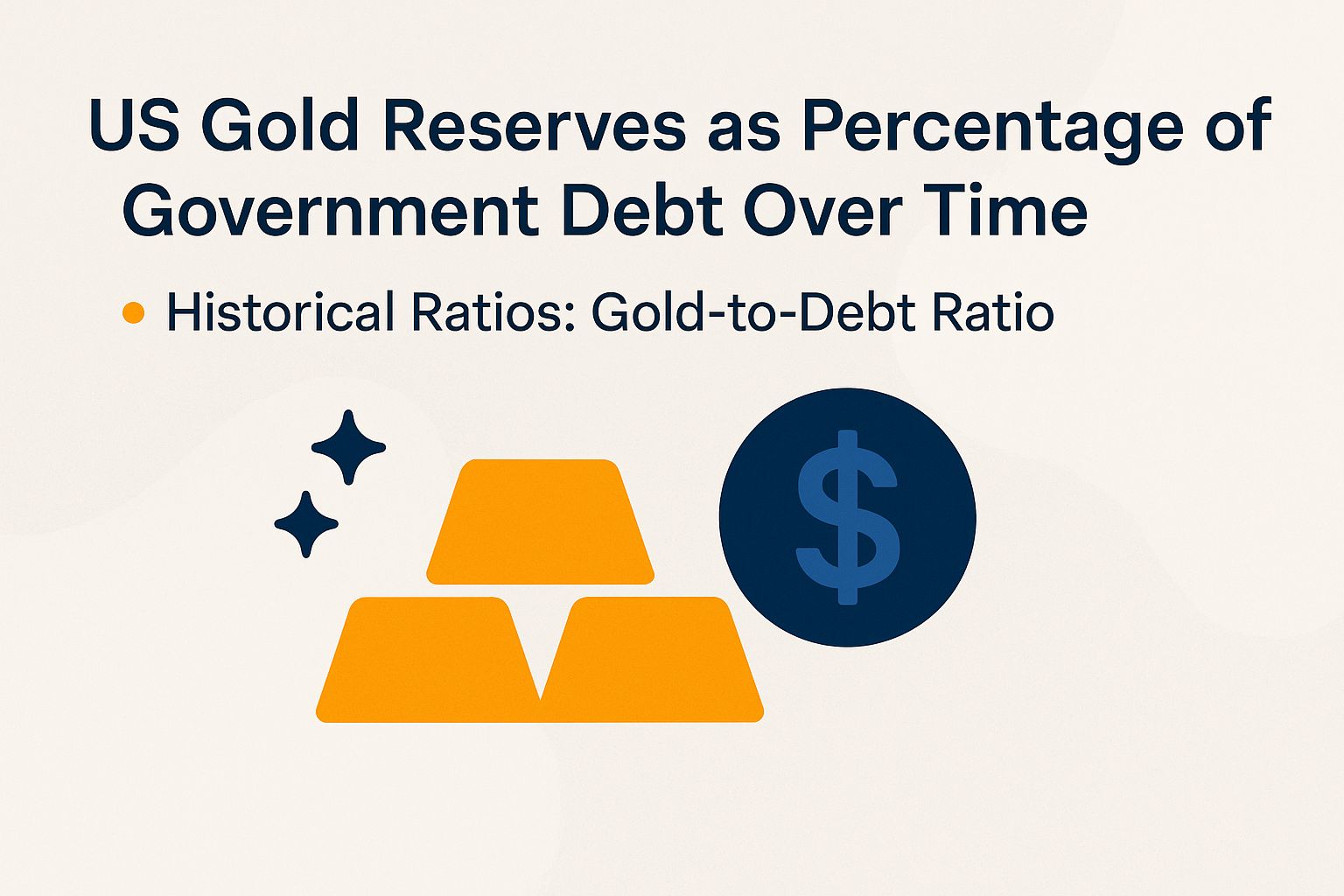

US Gold Reserves at Fort Knox vs. Government Debt Over Time

#wk7ipc27.bar-container { position: relative; overflow: visible!important; } #wk7ipc27.bar-value { position: absolute!important; left: 50%!important; top: 50%!important; transform: translate(-50%, -50%)!important; color: white!important; font-weight: 700!important; font-size: 14px!important; white-space: nowrap!important; background: rgba(0, 0, 0, 0.7)!important; padding: 4px 12px!important; border-radius: 20px!important; z-index: 30!important; text-shadow: 0 1px 2px rgba(0, 0, 0, 0.3)!important; pointer-events: none!important; display: inline-block!important; } #wk7ipc27.animated-bar { z-index: 1!important; } @media (max-width: 768px) { #wk7ipc27 { padding: 16px!important; } #wk7ipc27 h2 { font-size: 24px!important; } #wk7ipc27 h3 { font-size: 16px!important; } #wk7ipc27.bar-label { font-size: 12px!important; } #wk7ipc27.metric-card { padding: 20px!important; } #wk7ipc27.bar-value { font-size: 13px!important; padding: 3px 10px!important; } } @media (max-width: 480px) { #wk7ipc27 { padding: 12px!important; } #wk7ipc27 h2 { font-size: 20px!important; } #wk7ipc27 h3 { font-size: 14px!important; } #wk7ipc27.bar-label { font-size: 11px!important; margin-bottom: 6px!important; } #wk7ipc27.bar-value { font-size: 12px!important; padding: 2px 8px!important; min-width: 45px!important; text-align: center!important; } #wk7ipc27.bar-container { height: 36px!important; overflow: visible!important; } }

US Gold Reserves as Percentage of Government Debt Over Time

Historical Ratios: Gold-to-Debt Ratio

(function() { setTimeout(function() { var bars = document.querySelectorAll(‘[class*=”animated-bar-wk7ipc27″]’); bars.forEach(function(bar) { var width = bar.getAttribute(‘data-width’); if (width) { bar.style.width = width + ‘%’; } }); }, 100); })();

The US Gold Reserves as Percentage of Government Debt Over Time illustrates a dramatic decline in the proportion of gold reserves backing national debt. This reflects shifts in economic policy, global finance, and monetary systems since the mid-20th century.

This metric, known as the gold-to-debt ratio, measures how much of the government’s debt is theoretically covered by official gold holdings, valued at market prices. A higher ratio suggests greater perceived stability and asset backing, while a lower one highlights reliance on fiat currency and credit systems.

During World War II, the gold-to-debt ratio stood at a robust 40%. This showed the era’s strong adherence to the gold standard.

The U.S. amassed significant gold reserves-peaking at over 20,000 metric tons-through inflows from war-torn allies and domestic production. Government debt rose due to wartime spending but stayed relatively low compared to gold stockpiles.

This high coverage provided security and supported the dollar as the world’s reserve currency. The 1944 Bretton Woods system, which created the IMF and World Bank, relied on this. Economists see this time as one of fiscal discipline, with gold hedging against inflation and uncertainty.

- 1970s Decline to 17%: The ratio dropped to 17% during tough economic times from loose spending policies and oil price jumps. In 1971, President Nixon ended the dollar’s link to gold, a move called the Nixon Shock. Oil shocks, high inflation mixed with slow growth, and bigger deficits pushed debt up for social programs and military needs. Gold reserves stayed at about 8,133 tons. This shift led to floating exchange rates, revealing U.S. economy weaknesses. Gold prices soared as a safe alternative, now easy to buy via gold ETFs.

- Current Ratio at 2%: Today, the ratio sits at just 2%, showing huge changes in modern finance. U.S. gold reserves, mostly at Fort Knox, haven’t grown since the 1970s. But national debt tops $35 trillion, with the debt-to-GDP ratio over 130% from deficits, pandemics, and infrastructure costs. At $2,500 per ounce, gold covers only a tiny part of debts. Ricardian equivalence is an idea that people expect future taxes to pay off debt, so they save more now. This stresses trust in the dollar’s global power over physical gold.

This drop shows the move from a gold-backed economy to one based on trust, productivity, and demand for U.S. Treasury bonds. Get ready-concerns grow about long-term risks amid geopolitical tensions and inflation.

Critics like Ron Paul warn of dangers and push to end the Federal Reserve. Yet fiat systems offer flexibility, as some theories explain. Policymakers could diversify reserves or audit gold to build trust.

The trend points to America’s focus on innovation over commodities. Exciting digital options like Bitcoin and future central bank digital currencies join traditional assets.

Gold as a Hedge Against Debt Crises

Gold acts as a strong shield against debt crises. It holds value when paper money weakens.

In 2020, during the COVID-19 debt explosion, gold gained 24%. Meanwhile, the S&P 500 dropped 34% at first-talk about a lifesaver!

Historical Performance in Economic Downturns

- 2008 Crisis: Gold returned 5.5% from 2007-2011, beating Treasury bonds’ -3.6% real decline, per Morningstar, as debt doubled to $14 trillion.

- Post-Nixon Shock (1971): This ended Bretton Woods and the gold standard, leading to patterns where gold thrived in uncertainty.

- 1998 Asian Crisis: Gold rose 10% as regional debts spiked.

In the 2011 Eurozone debt crisis, gold gained another 10% amid extensive sovereign bailouts. The International Monetary Fund’s publication, Gold as an International Reserve Asset (1979), highlights gold’s critical role in stabilizing international reserves during periods of economic volatility.

| Event | Gold Return | Debt Impact |

|---|---|---|

| 1970s Inflation | +2,300% | Dollar -85% value |

| 1998 Asian Crisis | +10% | Regional defaults |

| 2011 Eurozone Debt | +10% | Sovereign bailouts |

For practical measures to safeguard against potential future debt crises, investors are advised to acquire physical bullion, such as 1-ounce American Eagle coins, from established dealers like APMEX, and to ensure secure storage of these assets.

Current Global Debt Landscape

The global debt landscape in 2024 totals $305 trillion, with emerging markets exhibiting a debt-to-GDP ratio of 250%, as reported in the International Monetary Fund’s April 2024 Fiscal Monitor. This escalation is largely attributable to borrowing in the aftermath of the pandemic.

A regional analysis reveals that the United States carries $34 trillion in debt, equivalent to 120% of its GDP, while China’s public debt stands at $14 trillion, or 80% of GDP, according to data from the People’s Bank of China. In Europe, the average debt-to-GDP ratio is 100%, per Eurostat figures.

For illustrative purposes, one might envision a world map color-coded by debt intensity: deep red shading for emerging markets, and amber for the United States and Europe.

Significant risks persist, including a 50% probability of default for Argentina, as assessed by Moody’s. The Bank for International Settlements’ Quarterly Review further cautions against the potential for financial contagion.

This situation bears resemblance to historical precedents, such as the United States’ debt-to-GDP peak of 150% during World War II.

In the current environment, gold has emerged as a reliable hedge, with prices rising 20% in response to inflation concerns, according to reports from the Institute of International Finance.

Implications for Economies and Investors

The escalation of government debt levels signals decelerated economic growth, though challenged by concepts like Ricardian equivalence. According to research from the International Monetary Fund (IMF), a 1% increase in debt as a percentage of gross domestic product (GDP) correlates with an annual reduction in economic growth of 0.02%. This dynamic incentivizes investors to diversify their portfolios by incorporating gold as a reliable mechanism for wealth preservation.

This debt accumulation engendering four primary implications for economies and investors.

- First, economies confront elevated interest rates, as evidenced by the US Treasury 10-year yield reaching 4.5% in 2024, according to World Bank data, which consequently raises borrowing costs across sectors.

- Second, inflationary pressures pose risks to purchasing power, eroding it by 2-3% annually as projected by the Congressional Budget Office (CBO), thereby amplifying gold’s role as an effective hedge against such erosion.

- Third, for investors, a strategic allocation of 5% to gold within a portfolio can mitigate volatility by 15%, based on JPMorgan analyses. Moreover, a $10,000 investment in gold from 2010 to 2020 generated a 50% return, outperforming bonds’ 20% return over the same period, in line with evaluations by economists Peter Schiff and Jim Rickards.

- Fourth, systemic vulnerabilities persist, reminiscent of the 2008 financial crisis and its associated $700 billion Troubled Assets Relief Program (TARP) bailouts.

In practical terms, investors are encouraged to commence exposure to gold through gold ETFs, such as GLD, to establish positions efficiently and with minimal complexity.

Future Outlook and Policy Considerations

Looking ahead, projections from the Institute of International Finance (IIF) indicate that global debt could reach $400 trillion by 2030. This escalation may propel gold prices to $3,000 per ounce should quantitative easing (QE) resume, particularly as central banks-such as Russia, which has repatriated 2,000 tons since 2014-continue to bolster their reserves.

This mounting debt burden raises profound concerns regarding economic stability, reminiscent of historical episodes like the Weimar Republic’s hyperinflation in 1923. During that period, the German mark depreciated from 4.2 to the U.S. dollar in 1914 to trillions by 1923, driven by unchecked money printing to finance war reparations.

Gold looks promising right now. High debt and renewed Quantitative Easing (QE, where central banks pump money into the economy) might weaken regular currencies and even digital ones like CBDCs. This makes gold a solid shield against rising prices, unlike riskier options like Bitcoin.

Look at the 2008 crisis as proof. Gold prices jumped 25% each year from 2009 to 2011.

This happened while the Federal Reserve’s QE programs grew its balance sheet by over $4 trillion.

Policymakers face tough choices, like austerity measures. The UK’s 2010 government tried austerity by cutting spending and raising taxes. It shrank the budget deficit by about 5% of GDP in five years.

This steadied finances after 2008. But it slowed growth and sparked public frustration.

Modern Monetary Theory (MMT) offers a different view. Economist Stephanie Kelton explains in her 2020 book *The Deficit Myth* that governments with their own currency can spend more than they earn without usual limits.

She says austerity hurts the economy. Japan has debt over 250% of GDP but no crisis, thanks to locals owning the bonds and low rates.

Experts disagree sharply, like libertarian economist Ron Paul pushes hard for the gold standard in his 2009 book *End the Fed*. He warns endless debt creates risky behavior and hurts savings-time to act before it’s too late!

Austrian economics agrees, as the Mises Institute teaches. It supports free markets and real money like gold.

They blame ups and downs in the economy on central banks meddling, per Ludwig von Mises’ 1912 book *The Theory of Money and Credit*.

Keynesian economics, backed by the Brookings Institution, loves government spending to boost recovery. A 2022 report shows COVID relief spending of $5 trillion prevented a deeper slump.

U.S. GDP bounced back 5.9% in 2021. But watch out-too much can fuel inflation.

To address these risks, three policy recommendations warrant consideration:

- Enforce Debt Ceilings: Establish rigorous statutory limits, as envisioned in U.S. bipartisan legislation, mandating congressional approval for debt exceeding 100% of GDP and triggering automatic spending reductions upon violation. This draws from Switzerland’s “debt brake” mechanism, which has constrained deficits to 0.5% of GDP since 2003.

- Conduct Gold Reserve Audits: Require comprehensive, transparent audits of holdings such as those at the U.S. Fort Knox facility (estimated at 4,580 tons). This mirrors Germany’s 2017 repatriation and verification of 1,236 tons from the New York Federal Reserve vaults, promoting accountability and countering allegations of manipulation.

- Impose Diversification Mandates for Pensions: Oblige public pension funds to allocate 5-10% of assets to gold and commodities, akin to the initiative in Texas’s $10 billion state fund in 2021. A 2023 study by *Pensions & Investments* indicates that such diversification yields 8% superior risk-adjusted returns during inflationary episodes by mitigating equity market volatility.

Investors, act now for a strong portfolio! Aim for balance with these steps:

- Put 5-10% in gold via easy options like the SPDR Gold Shares ETF (GLD).

- Spread the rest into bonds and stocks.

- Keep an eye on inflation signs like the Consumer Price Index (CPI).

Talk to trusted financial advisors right away. Stay updated via solid sources like the World Gold Council.

Gold protects against big shocks. But don’t go all-in-growth stocks shine in steady times.