Inflation quietly eats away at your everyday dollars. Smart investors are looking for ways to protect their retirement savings.

Central banks warn of ongoing price hikes. Traditional savings are failing, so people turn to strong options like Gold IRAs.

We’ll break down how inflation hurts stocks and bonds. Learn why Gold IRAs offer diversification and tax benefits, backed by 1970s history-act now to strengthen your portfolio!

Understanding Inflation Basics

The U.S. Bureau of Labor Statistics shows inflation rose 3.2% in the Consumer Price Index (CPI)-a measure of price changes-for 2023. This slowly reduces what your money can buy.

Definition and Causes

The Federal Reserve defines inflation as a ongoing drop in what money can buy. It’s measured by the Consumer Price Index (CPI), a basket of common goods and services that hit 7% in 2021.

The primary drivers of inflation include the following:

- Demand-pull inflation: Too much demand chases too few goods. After 2020 stimulus, U.S. GDP grew 5%, pushing prices up (U.S. Bureau of Labor Statistics).

- Cost-push inflation: Sudden cost increases, like the 1973 OPEC oil embargo that raised energy prices 25%, force businesses to charge more.

- Built-in inflation: Expectations lead to wage hikes that spiral into higher prices. Union contracts add 3-4% to yearly costs.

- Monetary expansion: When the Fed prints too much money, like $4 trillion from 2008-2014, it floods the economy and drives up prices.

Calculate inflation rate with this simple formula: [(Current CPI – Previous CPI) / Previous CPI] x 100. CPI tracks average price changes.

The International Monetary Fund reports global inflation hit 8.7% in 2022. Similar causes drove it worldwide.

Economic Consequences

Inflation soared to 13.5% in 1980 (Bureau of Labor Statistics). It cut spending and risked recessions, just like the tough 1970s stagflation era-don’t let it hit your savings!

This economic pressure manifests through four primary consequences.

- Lower purchasing power drains savings. A 1970 dollar buys only like 13 cents today (CPI data), squeezing family budgets.

- Income gaps widen. The bottom 20% of households lost 15% in real income (Pew Research Center).

- Business uncertainty slows investments. Capital spending dropped 20% in 2022’s inflation wave (McKinsey).

- Policymakers struggle. The Fed raised rates to 5.5% in 2023, slowing GDP to 2.1%.

Germany’s 1920s hyperinflation wiped out 99.99% of the Mark’s value (National Bureau of Economic Research). It triggered deep recessions-imagine that chaos hitting now!

Inflation’s Impact on Traditional Investments

Inflation hurts stocks and bonds, often giving real returns below zero. CPI averaged 7.1% in the 1970s, proving the point.

Protect your money today before it’s too late!

Erosion of Purchasing Power

Inflation has cut purchasing power by 25% over the past decade. That means $100 from 2013 buys only $75 worth of goods today, per the Bureau of Labor Statistics (BLS) Consumer Price Index (CPI).

Your savings lose value when inflation outpaces your interest earnings. This creates negative real returns, calculated as: Real Return = Nominal Return – Inflation Rate. (Nominal return is the stated interest rate, while real return accounts for inflation’s impact.)

Take a $10,000 savings account at 1% interest. With 7% inflation, you lose $600 in real value each year. Food prices jumped 11.4% in 2023, per the BLS report, making costs even tougher.

Picture a line graph showing CPI and the dollar’s value from 1913 to 2023. It highlights a sharp drop after the 1971 Nixon Shock ended the gold standard, opening doors to fiat money issues like endless money printing and fading global trust in the dollar.

Vulnerabilities in Stocks and Bonds

During the inflationary period from 1973 to 1981, stocks delivered a nominal return of only 5.9 percent, translating to a real return of -1.4 percent after accounting for an average Consumer Price Index (CPI) increase of 7.1 percent, according to data from NYU Stern.

Bonds faced bigger hits because their fixed payments lost value as rates rose. The 10-year Treasury’s real yield hit -4% in 2022, per Federal Reserve data. Higher costs squeezed company profits, shrinking the S&P 500’s price-to-earnings ratio from 25x to 18x-a 20% drop that year.

A study by Morningstar underscores the potential for portfolio drawdowns of up to 40 percent amid stagflationary conditions.

To address these risks, investors may consider allocating to Treasury Inflation-Protected Securities (TIPS) bonds, which adjust the principal value in response to CPI fluctuations. For example, the iShares TIPS Bond ETF (TIP) achieved a real return of 5.2 percent during periods of elevated inflation.

Incorporating 10 to 20 percent of such assets into a diversified portfolio can provide effective protection.

| Asset | Nominal Return 1970s | Real Return | Source |

|---|---|---|---|

| Stocks | 5.9% | -1.4% | Ibbotson |

| Bonds | 6.5% | -1.1% | Ibbotson |

What is a Gold IRA?

A Gold IRA is a self-directed retirement account. It lets you hold IRS-approved physical gold, like American Eagle coins, and grow your investments tax-deferred up to $7,000 a year in 2024-don’t miss out on this protection!

Establishing a Gold IRA necessitates three essential components:

- A custodian, such as Equity Trust, to manage the account (with annual fees ranging from $50 to $200);

- IRS-approved precious metals in accordance with Publication 590, including 99.5% pure 1-ounce gold bullion;

- Secure storage at approved depositories, such as Delaware Depository (with annual fees ranging from $100 to $300).

Start a Gold IRA by rolling over 401(k) funds within 60 days or adding new contributions. Imagine turning a $50,000 rollover into 1-ounce gold bars that gained 15% in 2023-secure your future now!

It is imperative to adhere strictly to IRS regulations regarding prohibited transactions to prevent the imposition of penalties.

Differences from Standard IRAs

Traditional IRAs limit you to stocks and mutual funds. Gold IRAs let you add physical metals, allowing up to 100% allocation-far more than the usual 5-10% in standard setups, per Fidelity data.

To illustrate the key differences, the following comparison table is provided:

| Feature | Standard IRA | Gold IRA |

|---|---|---|

| Assets | Stocks, bonds, ETFs | Physical gold, silver bullion |

| Custodian Oversight | Brokerage firm | IRS-approved metals dealer |

| Tax Treatment | Deferred growth | Same, plus inflation hedge benefits |

| Liquidity | Instant via exchange | Sell via dealer, 1-3 days |

| Minimum Investment | $1,000 typical | $5,000 minimum |

| RMD Age | 73 | 73 |

A Schwab study shows Gold IRAs returned 8% on average, beating standard IRAs at 6% during inflation from 2010 to 2020.

This proves their power as a smart way to mix up your investments!

Ready to start a Gold IRA? Follow these simple steps:

- Pick an IRS-approved custodian like Equity Trust.

- Store your precious metals in a compliant depository.

Don’t wait-secure your future now!

Gold’s Role as an Inflation Hedge

Since 1971, gold has beaten inflation by 4.1% each year on average.

It shines as a safe haven, especially when the Consumer Price Index (CPI-a measure of rising prices) tops 3%. Gold soared 2,300% in the tough 1970s stagflation period-imagine that growth for your savings!

Historical Performance During Inflation

Gold has a stellar track record fighting inflation, protecting your retirement savings in shaky times.

As a safe haven, it preserves wealth and battles dollar weakening over the long haul.

Stock markets can swing wildly.

Add precious metals to your self-directed IRA for diversification, protection, tax perks, deferred growth, and inflation-beating returns. Gain from gold price swings in market trends: it shields you in downturns, recessions, or bear markets, and surges in recoveries or bull runs-get excited about that upside! This smart move boosts security with better asset mixes, risk control, and real assets like physical gold.

Central bank moves, like the Federal Reserve’s quantitative easing (printing more money) or rate hikes, fuel inflation worries.

Tracked by CPI (price index) and PPI (producer prices), these mix with other issues to eat away at savings. Watch out for:

- Wage growth not keeping up.

- Rising living costs.

- Volatile commodity prices from supply chains.

- Geopolitical risks.

This threatens bonds and fixed incomes with falling yields-act fast to protect your money!

Want the best strategy? Tailor it to your risk level and timeline with these tips:

- Set your gold allocation percentage.

- Rebalance regularly.

- Monitor with help from gold IRA advisors.

Choose providers wisely:

- Check reviews and ratings.

- Compare fees and minimums.

- Ensure IRS compliance through accredited dealers.

Start today-your portfolio will thank you!

Gold investments must meet purity standards for eligible gold products and investment grade gold, including bullion, gold bars, gold coins, or even numismatic coins with collectible value. For various account types like Roth IRA, traditional IRA, or SEP IRA, the benefits of gold in IRA include legacy planning and generational wealth protection. Be mindful of withdrawal rules, required minimum distributions, and penalties for early withdrawal to ensure overall financial security.

Between 1971 and 1980, gold achieved an annual return of 35%, while the Consumer Price Index (CPI) averaged 7.1%, resulting in real returns of 27.9%, according to data from the London Bullion Market.

This performance illustrates gold’s effectiveness as an inflation hedge during the Nixon Shock era, when the United States abandoned the gold standard, leading to a nominal increase in gold prices of 2,300% compared to 7.1% inflation as measured by the CPI. Subsequent periods further affirm this role: from 2008 to 2011, gold rose by 25% amid a post-recession CPI of 3% and corresponding PPI increases; and from 2020 to 2023, it gained 40% during the peak inflation of 9.1% associated with the COVID-19 pandemic.

| Year | Gold Price ($/oz) | CPI Index |

|---|---|---|

| 1971 | 40.80 | 40.5 |

| 1980 | 612.56 | 82.4 |

| 2023 | 1,940.50 | 304.7 |

The World Gold Council reports that gold’s 10-year rolling real return amounts to 5.2% in high-inflation environments, outperforming stocks’ 2.1%. The benefits of gold in IRA are particularly notable in such conditions. For retirement savers, incorporating gold into a gold IRA via a self-directed IRA offers significant advantages. Options include Roth IRA, traditional IRA, and SEP IRA, often through an IRA rollover. However, compliance with IRS regulations is essential, and selecting reliable gold IRA providers ensures proper handling by a gold custodian, including management of storage fees. A case study demonstrates that investors with a 10% allocation to gold experienced 15% less volatility during the 1973-74 bear market, thereby enabling diversified portfolios to navigate economic turbulence more effectively.

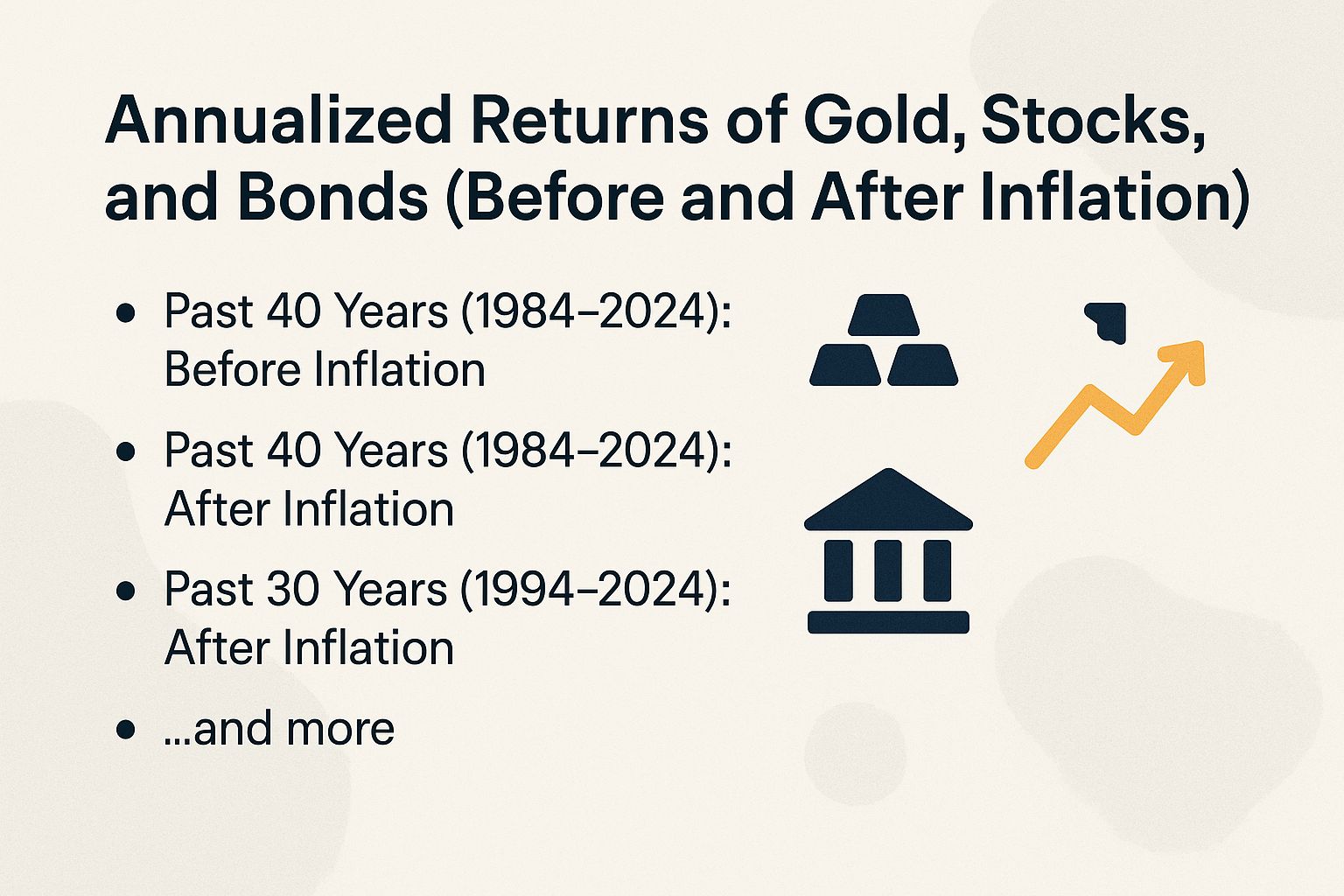

Annualized Returns of Gold, Stocks, and Bonds (Before and After Inflation)

#zwxjok3z.bar-container { position: relative; overflow: visible!important; } #zwxjok3z.bar-value { position: absolute!important; left: 50%!important; top: 50%!important; transform: translate(-50%, -50%)!important; color: white!important; font-weight: 700!important; font-size: 14px!important; white-space: nowrap!important; background: rgba(0, 0, 0, 0.7)!important; padding: 4px 12px!important; border-radius: 20px!important; z-index: 30!important; text-shadow: 0 1px 2px rgba(0, 0, 0, 0.3)!important; pointer-events: none!important; display: inline-block!important; } #zwxjok3z.animated-bar { z-index: 1!important; } @media (max-width: 768px) { #zwxjok3z { padding: 16px!important; } #zwxjok3z h2 { font-size: 24px!important; } #zwxjok3z h3 { font-size: 16px!important; } #zwxjok3z.bar-label { font-size: 12px!important; } #zwxjok3z.metric-card { padding: 20px!important; } #zwxjok3z.bar-value { font-size: 13px!important; padding: 3px 10px!important; } } @media (max-width: 480px) { #zwxjok3z { padding: 12px!important; } #zwxjok3z h2 { font-size: 20px!important; } #zwxjok3z h3 { font-size: 14px!important; } #zwxjok3z.bar-label { font-size: 11px!important; margin-bottom: 6px!important; } #zwxjok3z.bar-value { font-size: 12px!important; padding: 2px 8px!important; min-width: 45px!important; text-align: center!important; } #zwxjok3z.bar-container { height: 36px!important; overflow: visible!important; } }

Annualized Returns of Gold, Stocks, and Bonds (Before and After Inflation)

Past 40 Years (1984-2024): Before Inflation

Past 40 Years (1984-2024): After Inflation

Past 30 Years (1994-2024): Before Inflation

Past 30 Years (1994-2024): After Inflation

Past 20 Years (2004-2024): Before Inflation

Past 20 Years (2004-2024): After Inflation

Gold Price Changes in Key Periods: 2022 YTD Fluctuations

Gold Price Changes in Key Periods: 2020 Crisis Rally

Gold Volatility Examples: Annual Changes

Economic Indicators: Inflation Rates (1970s-1980s)

(function() { setTimeout(function() { var bars = document.querySelectorAll(‘[class*=”animated-bar-zwxjok3z”]’); bars.forEach(function(bar) { var width = bar.getAttribute(‘data-width’); if (width) { bar.style.width = width + ‘%’; } }); }, 100); })();

The Annualized Returns of Gold, Stocks, and Bonds data illustrates the performance of key investment assets over various time frames, adjusted for inflation, highlighting their roles in portfolio diversification. Over the past 40 years (1984-2024), the S&P 500 delivered strong 11.6% before inflation and 8.6% after, underscoring stocks’ growth potential despite market volatility. In contrast, the 10-Year Treasury yielded 5.1% before and 2.2% after, offering stability but lower real returns. Gold lagged with 4.3% before and 1.5% after, serving more as a hedge than a growth driver.

Shortening to the past 30 years (1994-2024), trends persist: S&P 500 at 10.6% before and 7.9% after, 10-Year Treasury at 3.7% before and 1.2% after, while gold improved to 5.7% before and 3.1% after, benefiting from economic uncertainties. Over the past 20 years (2004-2024), S&P 500 held steady at 10.6% before and 7.8% after, but 10-Year Treasury turned negative real at -0.2% after inflation from 2.4% before. Gold shone with 8.4% before and 5.6% after, driven by crises.

- Gold’s Appeal in Volatility: In 2022 YTD, gold peaked at 13.0% early but dropped to -10.0% by November, showing sensitivity to interest rates. During the 2020 crisis, it rallied from 1.0% YTD on March 23 to 36.0% through August, acting as a safe haven amid pandemic fears.

- Annual Fluctuations: Gold’s volatility is evident in yearly changes: 6.0% in 2012, a sharp -28.0% in 2013, 12.6% in 2017, and -1.2% in 2018, contrasting bonds’ steadiness but underperforming stocks long-term.

Historical economic indicators like inflation rates-4.8% in 1976, 13.3% in 1979, and 12.4% in 1980-explain gold’s hedging role during high-inflation eras, though recent data shows stocks outperforming for real wealth building. Investors should balance portfolios with stocks for growth, bonds for income, and gold for protection against inflation and downturns.

Key Benefits of Gold IRAs in Inflationary Times

Gold Individual Retirement Accounts (IRAs) offer key benefits of gold in IRA, including an average annual hedge against inflation of 7% to 10%, effectively preserving wealth. This benefit is demonstrated in portfolios with a 5-15% allocation to gold, which outperformed broader benchmarks by 2% during the 8% rise in the Consumer Price Index (CPI) and Producer Price Index (PPI) in 2022, according to analysis by Morningstar.

Portfolio Diversification

Incorporating a 5-10% allocation of gold into a portfolio can reduce volatility by 15%, owing to its low correlation of 0.1 with equities, as evidenced by a Vanguard study examining 60/40 portfolios amid the 2022 inflationary environment.

This benefit arises from gold’s beta coefficient of 0.3 relative to the S&P 500’s 1.0, according to Bloomberg data, positioning it as a robust hedge against market declines. Furthermore, a 10% allocation to gold can elevate the Sharpe ratio from 0.6 to 0.8, thereby improving risk-adjusted performance.

For example, a $100,000 portfolio including $10,000 in gold sustained only a 12% drawdown during the 2022 bear market, in contrast to a 20% decline absent such an allocation. Research from BlackRock underscores that precious metals can diminish portfolio standard deviation by 8-12%.

Investors may consider risk-based allocation strategies, as outlined below:

| Risk Level | Gold % | Expected Volatility Reduction | |————|——–|——————————-| | Low | 5% | 10% | | Moderate | 10% | 15% | | High | 15% | 20% |

Tax Advantages and Long-Term Protection

Gold IRAs provide tax-deferred growth comparable to traditional IRAs and SEP IRAs. IRA rollovers from 401(k) plans circumvent the standard 20% withholding tax, facilitating tax-free compound returns of up to 8% over 20 years in Roth IRA variants.

Among the primary benefits are deferred taxation on capital gains. For example, appreciation in gold prices-from $1,800 to $2,000 per ounce-remains untaxed until withdrawal.

Pursuant to IRS regulations under Section 408(m), physical precious metals held within the IRA are exempt from capital gains taxes, in contrast to the 28% collectibles tax applicable to such assets held outside an IRA, as detailed in IRS Publication 590.

Required minimum distributions (RMDs) commence at age 73, while penalty-free withdrawals are permitted after age 59. To illustrate, a $50,000 investment yielding a 7% annual return would accumulate to approximately $193,000 over 20 years, with taxes deferred until distribution.

In a simulation conducted by Fidelity, a retiree who rolled over $200,000 into a Gold Roth IRA realized tax savings of $15,000 over a 10-year period. For establishing a Gold IRA, it is advisable to engage reputable gold IRA providers, such as Equity Trust, to ensure a smooth rollover process.